Andreas Eriksson | 2022-09-29 10:00

Cancelled preference share issue

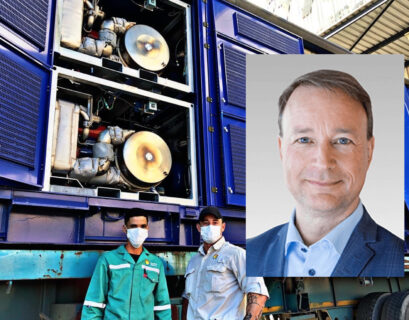

In the middle of the ongoing preference share issue, the board of Swedish Stirling decided to cancel the issue, citing market conditions. The issue was meant to finance the agreement with Glencore Merafe to provide a 10 MW energy conversion service based on PWR BLOKs to Lion Smelter in South Africa and as a consequence that deal now needs to be re-negotiated. Trying to sell the PWR BLOK, transferring technical and operational risk as well as financing to the buyer, is however a model that has already been tried, without any luck so far. But there are reasons to believe that the situation could be different this time.

Industrial case remains as clean energy remains a hot topic

As for the prospective customers, foremost Glencore, liquidity should not be an issue. Glencore, who was also an anchor investor in the planned preference share, reported a net income of USD 9.1b for 2021, while also setting aggressive environmental targets of a 50% total emissions reductions by 2035 and net zero by 2050. Therefore, there should be both environmental and economic incentives as well as financial muscles to invest in a technology that lowers both energy consumption and carbon emissions. These are also ambitions and demands that are not limited to companies in the South African ferrochrome industry. With that in mind, we remain optimistic about the technology and the chances for the investment case to materialise into firm system sale deals.

Elevated near-term risks

We no longer expect deliveries to Lion Smelter before year end, as any potential new agreements will likely take time, thus pushing first revenues further into the future. A valuation model based on 20% WACC indicates that today’s share price of SEK 6 reflect an expectation of a rollout amounting to 16 MW by 2026. For our base case we now forecast 2 MW sold in 2023 and a total of 22 MW installed by 2025, which hinges on firm sales deals singed by end H2’23 at the lastest. Using a combined target multiple and DCF (WACC 20%) approach, we now find support for a fair value range of SEK 9 – 12, and see a re-negotiated deal with Glencore, or other firm sales deals as the key triggers short-term. Should the company be able to reach agreements sooner rather than later, a rollout of the full 96 MW pipeline in South Africa by 2027 would instead imply a value of SEK 16-20 per share.

DISCLAIMER