Andreas Eriksson & Johan Widmark | 2022-05-16 14:00

Financial model that continues to evolve

The production line in Sibbhult is now complete and Swedish Stirling now targets delivery of 6 PWR BLOK units to Lion before year end, with a gradual increase in production rate. By its unique proprietary solution for recovering energy from industrial residual and flare gasses and converting these into 100% carbon neutral electricity at high efficiency, the 10 MW installation on Glencore’s Lion will generate up to 87,500 tonnes in annual CO2 emissions reduction. While the use of PWR BLOK in South Africa will entitle the owner to emission allowances equal to the amount of CO2 emissions saved, Swedish Stirling is now examining the possibility to not resell the allowances, but to tie the CO2-reduction to the planned preference share issue of 130 MSEK.

This unique green preference share is planned to offer both an attractive direct return paid in quarterly coupons, while also offering investors the possibility to offset emissions. Being a previously untested model, we are eager to see both terms and the response from the investor community. Combined with the debt financing agreement from The Industrial Development Corporation of Africa, this would give Swedish Stirling a robust financial platform to scale production.

Changing macro setting not affecting plan or execution

With a contracted revenue for Lion of SEK 413 million with a back-end loaded spread over 8 years, plus a 7-year extension option, we estimate a total discounted net present value of 9 MSEK per PWR BLOK for the ordinary shareholders, although rising inflation, risk premiums and financing costs are likely to dent that number. However, considering that it’s normal for South Africa to run at an inflation rate that’s elevated compared to European levels, this will not affect the company’s plan.

New deals now under negotiation will likely be financed with a higher degree of debt, hopefully not requiring the company to use its ~200 MSEK cash pile for project financing. A straightforward extrapolation of our calculation for the Lion deal to Swedish Stirling’s whole 96 MW pipeline of signed and potential energy conversion deals corresponds to a total value of SEK 2.2 billion or SEK 17 per share, without regard to falling production costs or additional potential outside existing letters of intent.

Several triggers support fair value well above today’s level

Aside from financing and the preference share issue, fixed agreements with the two remaining ferrochrome producers in South Africa and the next step with SMS Group in Europe are now two major triggers for the share. We also note the possibility of a verification of the environmental benefits PWR BLOK creates, through an independent review. Since PWR BLOK in South Africa reduces more carbon dioxide per invested SEK than any other comparable type of energy, a sustainability certification together with the preference share and a potential move to the main list, would force the company onto the radar screen of a number of indices and institutional sustainability investors in Sweden and internationally.

Now focus is on delivering and scaling up installations on Lion Smelter and signing new agreements with Samancor and Richards Bay Alloys, as well as SMS Group in Europe. So, with a number of triggers in 2022, support from the CEO’s acquisition of 204,000 shares in Q4’21 and recent purchase by Chairman Sven Sahle of 84,600 shares (increasing his holding by less than 1%), a possible sustainability certification and more potential deals in the pipeline, we now see considerable revaluation potential in the share.

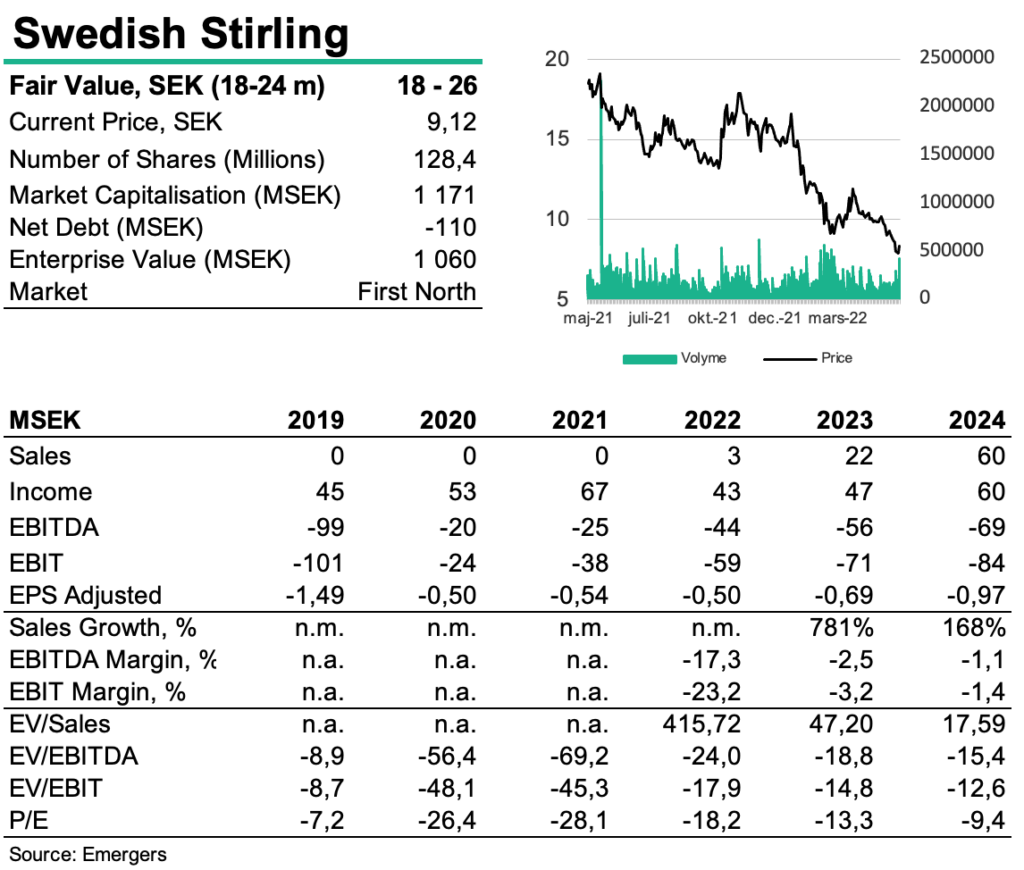

However, while the case in Swedish Stirling remains intact, the valuation is not insulated from the general downturn in market conditions and heightened risk premium with a special disapproval among investors for profitability far ahead in the future, which is why our combined DCF and multiple valuation now support a fair value of SEK 18-26 (26-36) in 18-24 months.

DISCLAIMER