The strategic partnership with Lonza puts Simris in a stronger position going forward as it both validates Simris IP in the high value Antibody-Drug Conjugate (ADC) space and moves the company closer to licensing deals, where we see opportunities for large revenues even in the short term. Encouraged by the deal, we continue to find support for a fair value of SEK 170-230m, which translates to SEK 0.94-1.28 per share in 12-24 months.

Andreas Eriksson & Johan Widmark | 2023-03-06 12:00

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and Emergers is not subject to any prohibition on dealing ahead of the dissemination of investment research. This research does not constitute investment advice and is not a solicitation to buy shares. For more information, please refer to disclaimer.

Lonza partnership validating Simris ADC platform

What started with the acquisition of Cyano Biotech GmbH (now Simris Biologics GmbH), bringing an ADC-payload platform with it, Simris has now taken the next step in pursuing the highest value verticals in the microalgae and cyanobacteria space. The partnership deal means that Lonza Ltd will become Simris’ Contract Development & Manufacturing Organization (CDMO) with global and exclusive rights to promote its ADC technology to biopharmaceutical companies. Lonza will integrate Simris’ ADC payload platform into its Bioconjugation Toolbox and offer the tech to customers seeking payloads to develop ADC medicine. Whilst Lonza will introduce Simris’ ADC payload technology to drug development companies any license deal will be directly between Simris and the drug developer. Due to the high value of such licensing deals within the fast-growing segment of ADC medicines, we see as a strong validation that is Simris moving in the right direction.Forecasting a sharp rise in revenues

ADC medicines have been recognized as effective, stable and reliable cancer therapeutics, and in 2022 alone, over 210 clinical trials involving ADCs were initiated. Strengthened by the Lonza partnership, there are highlights to look out for also in the shorter term. Simris’ new Omega-3 product is about to launch in the US on Amazon platform providing a platform for near term revenue. The photobioreactors were shut down and upgraded during the winter, putting the development work around Simris’ Fucoxanthin product for B2B sale on pause. Now that they are again up and running again we expect the refined and expanded B2B-offering, will enable Simris to grow topline substantially in the second half of the year.Positive momentum, with significant further upside potential

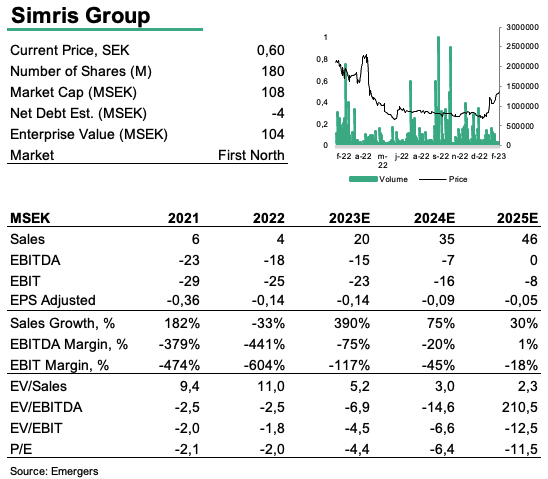

With a strong structural foundation in place and a clear strategy with a distinct roadmap for each of the verticals, we believe Simris is well positioned for an eventful year ahead. Based on a fraction of listed peer multiples, we continue to find support for a fair value of SEK 170-230m in 12-24 months, which translates to SEK 0.94-1.28 per share. We also note that an ADC platform licensing deal would boost potential further, and that big steps towards that end is now being taken.

DISCLAIMER