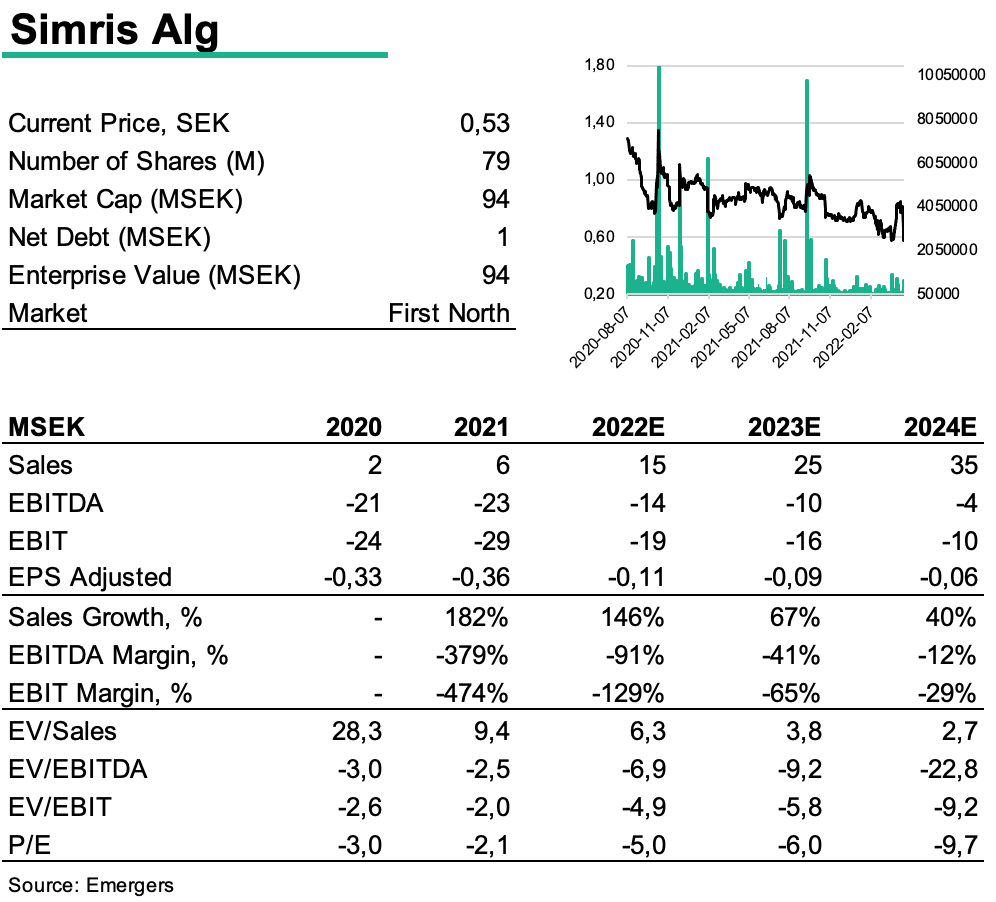

A refreshing wind of change

After 7.5 MSEK in orders during the last eight months Simris is now seeing the first fruits of the strategic transformation initiated by the Board and the final two pieces of the puzzle just about to fall into place. Julian Read, appointed new CEO effective 16th May, brings relevant experience from both sales and marketing in the cosmetics and pharmaceutical segment. Simris products are all based on precision-farmed microalgae and target a large and growing market in nutrition, skincare, and biopharma. With the improved room to manoeuvre after the rights issue, the company will target four B2B revenue streams, Novel Foods, Biomimetics, Simris and R&D-as a Service, which the Board have identified as segments with great potential.

Broaden business model with R&DaaS

The algae in Simris’ farm have been refined by eleven years of natural selection which has optimized its performance and the concentration of valuable nutrients. During Q1’22 Simris has invested to strengthen R&D, with the conduction of a hot-water extraction in search for skincare actives. The actives will be evaluated and tested to develop claims, which are key to monetize the ingredients in the skincare industry. In 2019, the market for active ingredients was estimated to be worth 2.2 BN USD with a CAGR at 7% in 2019-2024E largely driven by product innovation, which Simris plans to tap into.

While most of the hard work on cost cutting has been done in 2021, the company aims to make further efficiency improvements and if Julian Read can maintain the momentum while expanding gross margin, broaden the business with a R&D-as a service and increase sales of fucoxanthin, we estimate Simris to show a positive EBITDA 2025E, but note that this estimate might prove too conservative as we see a fair chance for the new CEO to accelerate above our expectations.

25 MSEK to accelerate momentum

Subscription period for the rights issue runs from April 21th – May 5th with a subscription price of 0,32 SEK per B share, which is a deep discount from current stock price. The issue will provide the company around 21 MSEK after costs and add 97,2 million new shares including the offset issue of 18 million shares from a conversion of a 6 MSEK bridge loan, which represents a dilution of 55% for non-participating shareholders. Notably, 80% of the rights issue is covered by subscription and guarantee commitments. Should some portion of the issue end up in the hands of guarantors this would present a palpable risk of hampering the share price performance in the short term.

In summary, we continue to see a significant revaluation potential in Simris, and that the triggers are now starting to line up, not least the prospects of Simris announcing claims in the skincare actives segment, in addition to ramping up sales of fucoxanthin. Applying a 6x sales multiple to our forecast (derived from a fifth of the sales multiple of only listed competitor Fermentalg) we find support for a fair value of 150 MSEK in 2023 and 210 MSEK in 2024, which translates to 0.85 SEK and 1.19 SEK per share in 2023 and 2024 respectively, assuming full subscription of the rights issue.