Johan Widmark | 2023-11-30 08:00

Stable sales in H1’23/24

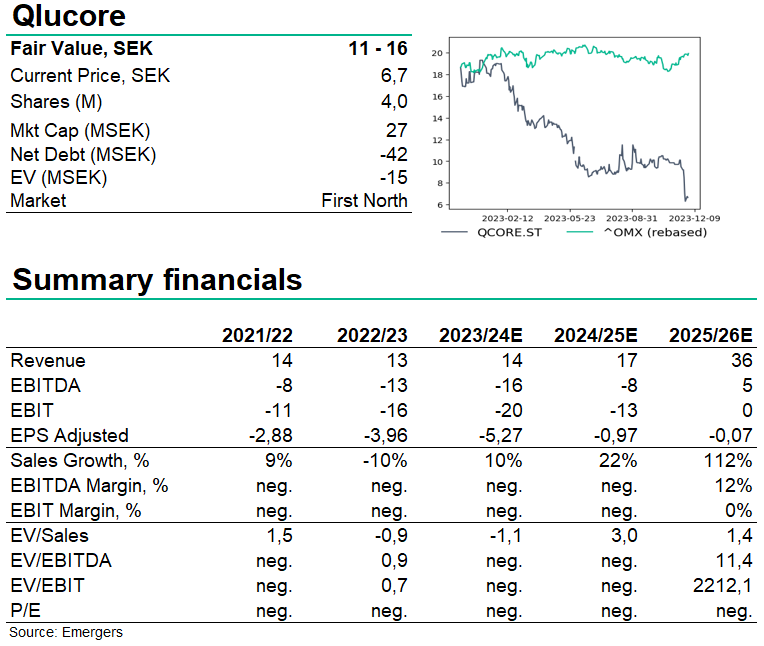

In Q2’23/24, Qlucore reported sales of SEK 2.9m, representing an 8% decline adjusted for FX. However, following the strong growth in Q1, organic sales growth in H1’23/24 was 5%. While OPEX came down sequentially, to SEK 12.8m in Q2, costs are still up YoY. The development work is now approaching the next phase, and combined with a cost-reduction plan, management expects OPEX to be significantly lower in 2024/25. Cash is now at SEK 45.6m following a net cash flow of SEK -11.6m in Q2’23/24.

Threefold CE approval in February 2025

With regards to Qlucore Diagnostics, focus is now the most common form of cancer in children, acute lymphoblastic leukemia (BCP-ALL). This will be followed by adult leukemia, bladder cancer, and lung cancer, thus covering 18% of all cancers, implying a considerable total market potential. Target is now set on the CE marking according to the IVDR regulations, expected in February 2025. This process covers three sub-projects, the Qlucore Diagnostics software, the specific model for acute lymphoblastic leukemia and the associated mandatory quality system. With development work expected to culminate in Q3’23/24, this will be a major driver for the cost reduction expected in 2024/25.

Support for sales of SEK 300m in 2028/29

We maintain our forecast of Qlucore Diagnostics and ALL approval in early 2025, with a subsequent increase in the number of labs to 70-100 labs by 2028/29. With an estimated number of tests per lab at 2,500-4,000 per year, and an estimated price per test of SEK 1,000, we find support for the company’s sales target of SEK 300m and a 40% EBIT margin, by 2028/29. In the short term we expect that Qlucore, despite its more concentrated focus and lowered cost base, will need to raise some SEK 50m before it is cash flow positive. But the continued decrease in the share price affects the likely terms of a future raise and adjusted for a SEK 50m rights issue at a 25% discount, we now find support for a fair value at SEK 11-16 (16-21) per share. We now see a) more visibility on future financing options, b) new license sales, and c) the first Diagnostics sales as the key catalysts for the share.

DISCLAIMER