Johan Widmark | 2022-11-30 08:00

Demand unaffected by business sentiment

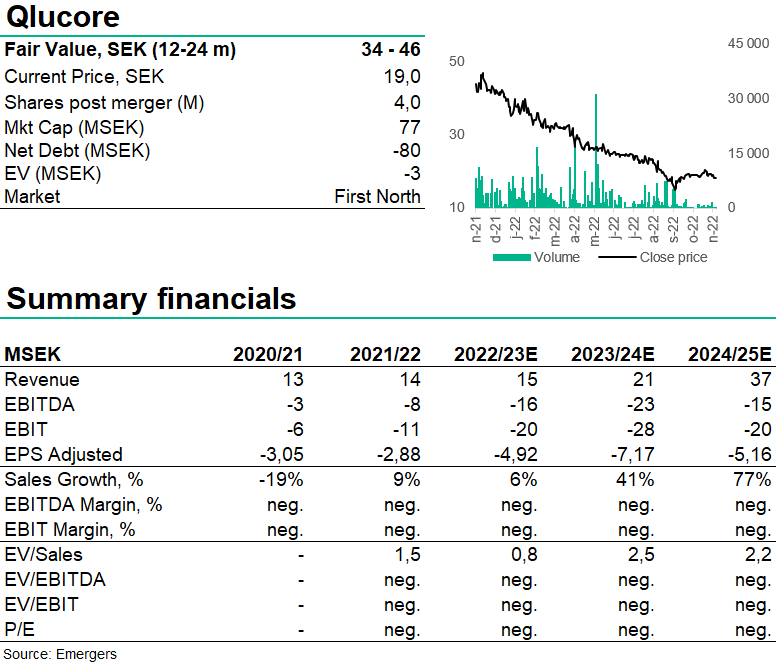

Net sales in Q2’22/23 amounted to 3.0 MSEK, exactly in line with our forecast. Despite a slowdown of 9% in Q2 (-17% adjusted for FX), which is within normal quarterly fluctuations as the sales mix between new deals and renewals shifts between quarters, sales in H1’22/23 are up 16% (4% adjusted for FX), confirming that the demand for Qlucore Omics Explorer is in fact resilient to a slower general business cycle and sentiment.

New project outside oncology

As planned, Qlucore continues to invest heavily in cancer diagnostics tools Qlucore Insights and Qlucore Diagnostics, the two software platforms offering AI-based machine learning for multi-omics companion and precision diagnostics with tailored classification models to help create individually adapted treatment for different types of cancer.

I addition to the partner funded development of models for the diagnosis of lung cancer, breast cancer, bladder cancer, and leukemia (ALL and AML), Qlucore has also announced a development grant from Vinnova of approximately 1.5 MSEK for the development of preventive precision medicine solutions for cardiovascular diseases. This project will run for three years and while the prospects for this project are less clear that for the oncology models, it is an interesting expansion of the long-term scope and potential for Qlucore’s technology.

Trading well below cash

We maintain our base case of a CE approval for the Qlucore Diagnostics platform and ALL in 2024, with a subsequent increase in the number of labs to 70-100 labs by 2027/28. With an estimate of the number of tests per lab at 2,500-4,000 per year, and an estimated price per test of 1,000 SEK, we find support for the company’s sales target of SEK 300m in 2027/28 and a 40% EBIT margin.

With three years of estimated losses (2022/23-2024/25) at a total 70 MSEK before turning to profit in 2025/26, our model supports the management’s claim that the SEK 80m net cash position will be enough to reach profitability. The stock now trades well below net cash and based on a combined DCF and multiple valuation we find support for a fair value of 34-46 SEK in 12-24 months, leaving plenty of upside from today’s level. Interestingly, our fair value range overlaps the subscription price in the management’s warrant program at SEK 45 in Nov 2025. We now see a) progress and visibility on the CE application process, b) new Qlucore Insights and Qlucore Omics Explorer license sales, and c) eventually first Diagnostics sales as the most important catalysts for the share.

DISCLAIMER