Johan Widmark & Magnus Brolin | 2022-05-13 09:30

Fundamental progress amid downturn

While the medtech and biotech sectors has taken severe beatings on the stock market in 2022, there has been some noteworthy progress for companies in Qlucore’s corner of the industry. In the beginning of Q1’22, American biotech Illumina signed a multi-year partnership with Agendia N.V., a company focussed on precision oncology for breast cancer, to advance the use of next generation sequencing for decentralized oncology testing for breast cancer patients. During Q1’22, precision medicine company PierianDx, announced a partnership with Biodesix to provide an interpretation technology platform to use with Biodesix genomic test to detect non-small cell lung cancer (NSCLC). Also, during 2022, laboratory company Aglient expanded its CE-IVD Mark for companion diagnostics to three new cancer indications. While these advances among Qlucore’s peers reflect an increasing competitive pressure, it also shows how the whole field of precision and companion diagnostics is progressing to develop a new generation of cancer treatments, for the benefit also of Qlucore.

CE and classification model for ALL in 2023

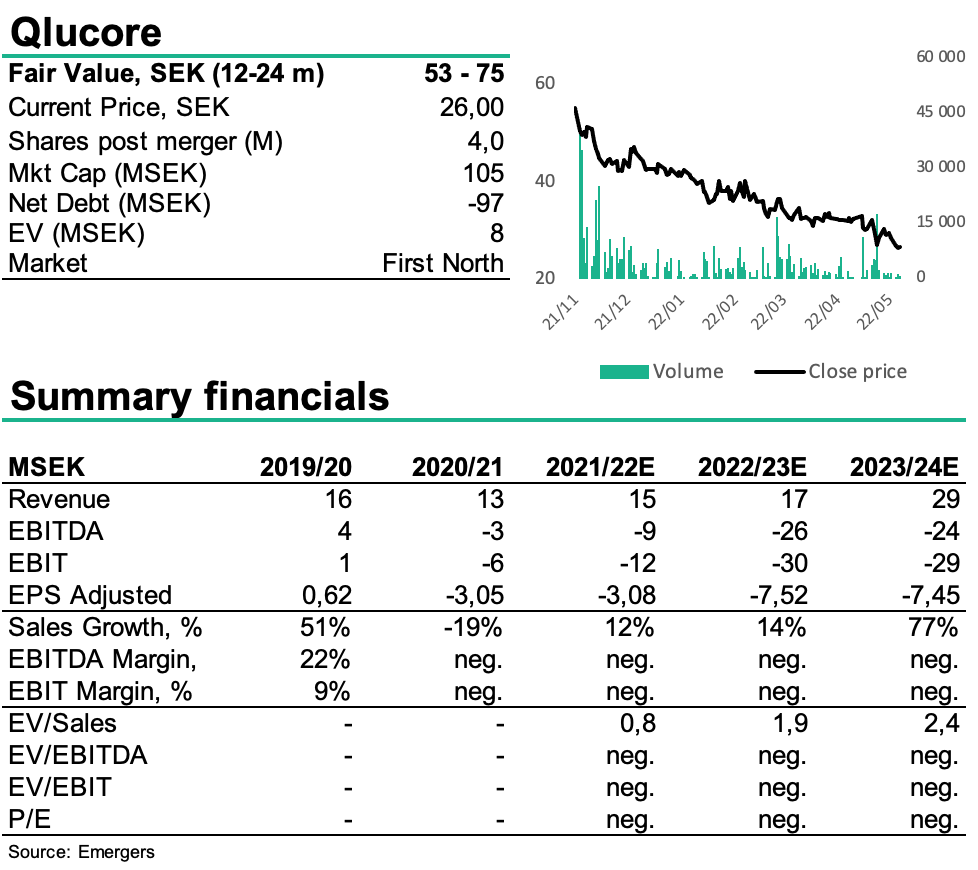

As for Qlucore, we expect the 53% growth in Q3’21/22 to taper off, before the development of tailored classification models for individualized treatment for different types of cancer can be converted to revenues. Following CE approval for Diagnostics’ basic platform and the classification model for ALL about a year away, we expect an increase in the number of labs to about 70-100 labs in 2026/27. As the company adds CE-approved tests for Non-small cell lung cancer (NSCLC) and breast cancer, we expect an increase in the number of tests per lab to 2,500-4,000 per year, which with an income of SEK 1,000 per test provides support for the company’s goal of sales of SEK 300 million 2026/27 and a 40% EBIT margin. With a continued decline in sequencing costs, demand for Qlucore’s services can be expected to increase. However, while the case in Qlucore remains intact, Qlucore’s valuation is not insulated from the general downturn in market conditions and heightened risk premium with a special disapproval among investors for profitability far ahead in the future, which is why our combined DCF and multiple valuation now support a fair value of SEK 53-75 (89-121) in 12-24 months.

DISCLAIMER