Johan Widmark | 2024-05-10 08:00

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and Emergers is not subject to any prohibition on dealing ahead of the dissemination of investment research. This research does not constitute investment advice and is not a solicitation to buy shares. For more information, please refer to disclaimer.

Anti-inflammatory combo and mAbs

Working with long-acting injectables Nanexa has had to deal with skin reaction at the injection sites on patients, which in the case of NEX-18 forced a halt of the Phase I study in September 2021. At the CMD, Nanexa now detailed how combining the injection with an anti-inflammatory drug have successfully reduced these skin reactions. The CMD also provided insight into the partner projects, where Nanexa conducted 7 preclinical studies in 2023, in addition to 7 preclinical studies for its own projects. Now half of projects are for monoclonal antibodies, around 1/3 for peptides and rest are small molecule. A review of the partner projects also showed that PharmaShell, in the finalized projects, have produced successful results, but that the projects were either under review or had been deprioritized for reasons outside Nanexa’s control.

NEX-22 and Novo project the most promising opportunities

The most interesting and promising opportunity in Nanexa is of course the interlinked NEX-22 project and the partner project with Novo Nordisk (that is also Nanexa’s largest shareholder at just shy of 20% of shares). For NEX-22, we anticipate that a successful Phase I and Ib/II trial would pave the way for out-licensing opportunities, potentially unlocking a total deal value estimated between USD 300 million (Xplico estimate, with the majority coming from upfront payments and milestones) and USD 800 million (the high end of our estimate, where royalties would constitute a larger part). This could justify an upfront payment of USD 40 million, assuming a 5% peak market share. The fate of NEX-22 is however interlinked with the outcome of the Novo Nordisk evaluation project, which is ongoing and scheduled to be concluded in 2025. Meanwhile, the timeline for NEX-22 aims to complete Phase 1b and have a Pre-IND meeting with the FDA by the end of 2025, in the best-case scenario.

Wide range of potential outcomes

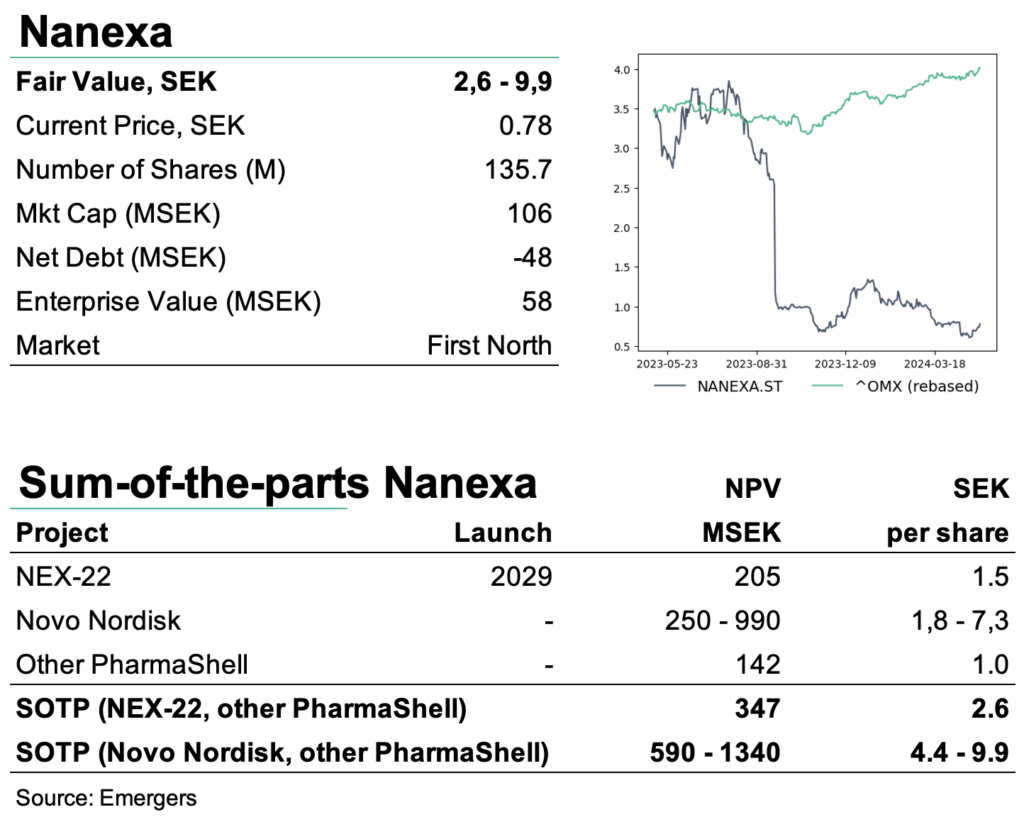

With cash at SEK 48m at the end of Q1’24, Nanexa expects to have runway into mid-2025. Based on our SOTP for NEX-22, the Novo Nordisk project and the PharmaShell evaluation deals, we continue to find support for an rNPV of SEK 2.6-9.9 per share. This wide range reflects the wide range of potential outcomes for the company’s various projects and partnerships. We now look forward to the start of Phase I with NEX-22 and more positive news flow from the partner projects as triggers in 2024.

DISCLAIMER