Johan Widmark | 2023-12-21 08:00

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and Emergers is not subject to any prohibition on dealing ahead of the dissemination of investment research. This research does not constitute investment advice and is not a solicitation to buy shares. For more information, please refer to disclaimer.

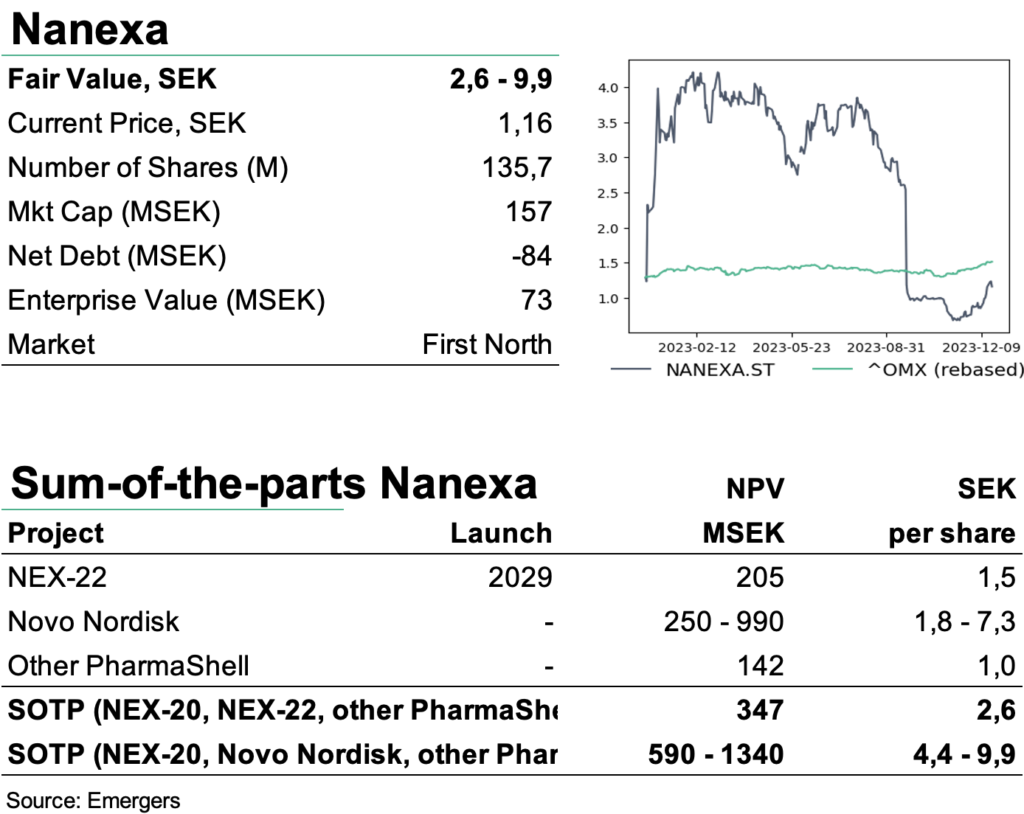

Close to a pure GLP-1 play

The three focus areas that will be prioritized going forward are:

• The own project NEX-22: A one-month depot of the GLP-1 substance liraglutide, within the large and very expansive type 2 diabetes indication. Nanexa now plans to start a clinical phase I study with NEX-22 in Q1 2024 with expected read-out at the end of 2024.

• The partner project with Novo Nordisk: The exclusivity and evaluation agreement covers Nanexa’s drug delivery system PharmaShell together with a specific substance class, not yet announced.

• Other well advanced partner projects where Nanexa sees opportunities for interesting broadening of collaborations with significant revenue potential during the period.

Clinical Trial Application for NEX-22 validated by EMA

Along with the announcement of the tactical reprioritization, Nanexa also announced that the Clinical Trial Application for the Phase I study of NEX-22 in patients with type 2 diabetes has been received and validated by the European Medicines Agency (EMA). This follows the results from the preclinical study of NEX-22 in minipigs confirming the long release profile of liraglutide, also seen in rats. Now Nanexa targets to start the Phase I study based on an approval in the first quarter of 2024.

Runway into 2025

With a cash position of SEK 84m after Q3 and the rights issue, the reprioritization will extend the company’s runway into mid-2025. But we also note a heightened pressure on the company to reach some form of licensing agreement in either of these three prioritized areas during 2024. After a revision of our SOTP, where we exclude NEX-20 for the time being, we now see support for a total rNPV of SEK 2.6-9.9 (4.3-11.6) per share. We continue to see a wide range of potential outcomes for the company’s various projects and partnerships and now look forward to the Phase I trial with NEX-22 and more positive news flow from the partner projects as triggers in 2024.

DISCLAIMER