Johan Widmark | 2023-10-11 08:00

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and Emergers is not subject to any prohibition on dealing ahead of the dissemination of investment research. This research does not constitute investment advice and is not a solicitation to buy shares. For more information, please refer to disclaimer.

Two scenarios depending on capital raised

At the investor meeting for the right issue, Nanexa presented two sets of milestones or scenarios going forward for the three own projects, NEX-18 (a long-acting injectable for treatment of myelodysplastic syndrome), NEX-20 (for multiple myeloma) and NEX-22 (for type-2 diabetes). One scenario if they manage to raise only the guaranteed amount of SEK 75m and one if they manage to raise the full SEK 121m. Significant emphasis was put on NEX-22.

In the SEK 75m scenario, the money will be enough to finance the completion of Phase 1 with NEX-22 and subsequent FDA meeting, preparation for Phase 1 with NEX-20, but no activities with NEX-18. Should they manage to raise the full SEK 121m, they will manage to start Phase 2 with NEX-22, start Phase 1b with NEX-20, and also an efficacy superiority study and preparations for Phase 1b with NEX-18.

Nanexa also aims to broaden PharmaShell for use in biological medicines, e.g. peptides and monoclonal antibodies, and conveys a lot of confidence in the possibility for a firm deal with its largest shareholder and evaluation partner Novo Nordisk.

Wide range of outcomes

At the investor meeting a lot of emphasis was put on NEX-22 which is a long-acting depot formulation of GLP-1 agonist liraglutide. Liraglutide is currently available as a once-daily injection, but NEX-22 is designed to be injected once a month, meaning a significant improvement in convenience for patients, and adherence.

This runs in parallel with Nanexa’s evaluation agreement with Novo Nordisk for an unspecified target. Our base-case assumption is that this is most likely other GLP-1 Semaglutide, now accounting for over 1/3 of Novo Nordisk’s revenues, with very positive growth prospects. In Q2’23, 45% of Novo Nordisk’s revenues were for some GLP-1 drug. We now see a 30% probability for a license deal with Novo Nordisk, estimating a 3% royalty fee in such a deal. A rough assumption of the application of PharmaShell on 10%-40% of Novo Nordisk’s portfolio corresponds to a SEK 250m -1bn NPV for the Novo Nordisk deal alone.

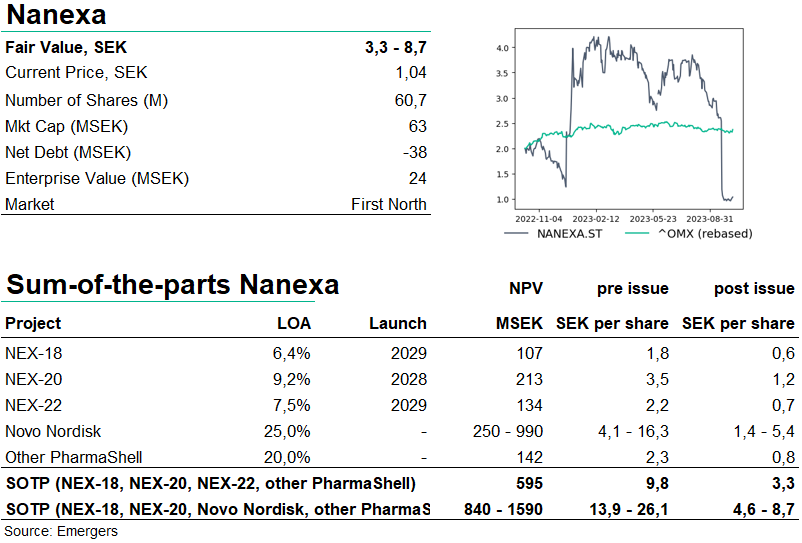

We now see a wide range of outcomes for the company’s various projects and potential partnerships. In our Sum of the Parts valuation, this gives support for a valuation range anywhere between SEK 600m and 1.6bn, corresponding to SEK 3.3-8.7 per share post issue. However, should the raise fall short of the SEK 121m target, this will also affect our SOTP, primarily with regards to NEX-18.

DISCLAIMER