Johan Widmark | 2022-06-13 08:00

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and Emergers is not subject to any prohibition on dealing ahead of the dissemination of investment research. This research does not constitute investment advice and is not a solicitation to buy shares. For more information, please refer to disclaimer.

New facility up and running

While the inauguration of Nanexa’s new premises showed both the high class GMP classified facilities as well as a confident board and management, the event did not provide any news. The benefits of Nanexa’s solution center around the improvements in patient compliance, comfort and cost reduction associated with long acting injectables, while to a varying extent relying on the original drugs’ documentation on efficacy etc. While our view and valuation remains based on seeing the proprietary projects through to Proof-of-Concept in phase II, Nanexa is continuously looking at minimizing what Proof-of-Concept would actually need to include. This leaves room for a small chance of finding a license deal after safety, tolerability and PK profile in phase Ib, rather than going through a full phase II alone. This would reduce the financial upside somewhat but also shorten the lead time to de-risk the case which would be beneficial for shareholders.An eventful year ahead

With the initiation of phase I with NEX-20 (a long acting injectable of lenalidomide for the treatment of multiple myeloma) in Q4’22, the announcement of a third proprietary project before year end 2022 (potentially a biological drug) and the restart of clinical trials of NEX-18 in 2023, we expect an eventful period ahead. While the new facility will increase costs going forward, we believe it will have a positive effect on the chances for a platform licensing deal for PharmaShell. This would moderate the need for additional financing while also providing an important reference point for the value of the platform, and most likely work as a positive trigger for the share.Support for a fair value of SEK 6.3-7.7 per share

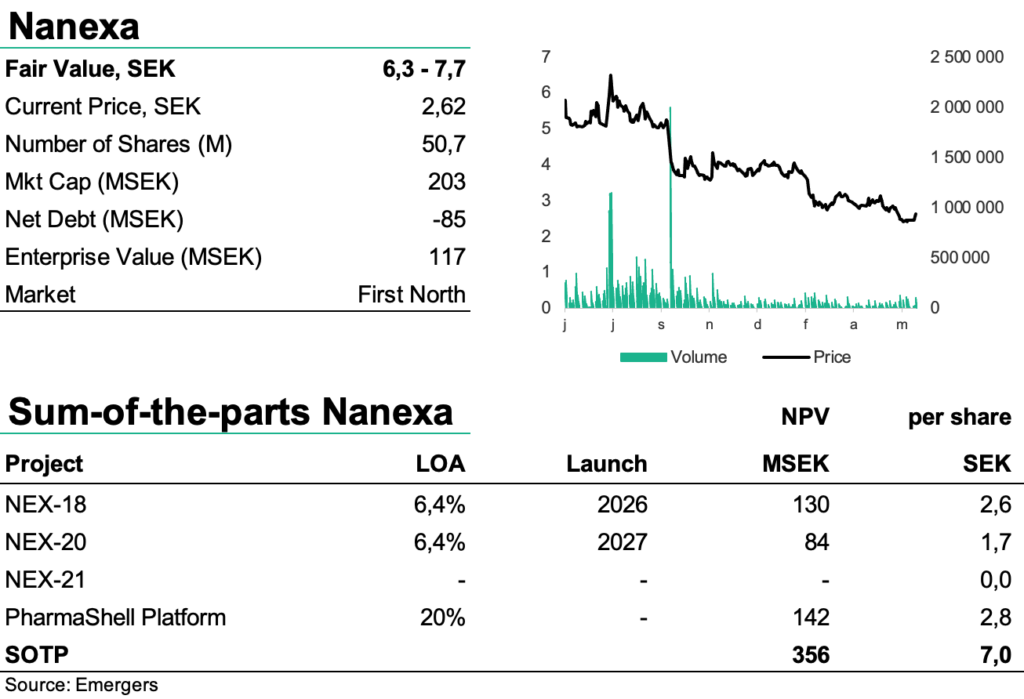

At the end of Q1’22 net cash amounted to SEK 85m, which is expected to finance the continued development into H1 2023. All in all, we see an accumulated probability for the company’s two preclinical projects of 6.4% from pre-clinic to approval, which with a risk-adjusted NPV for NEX-18, NEX-20 and the platform PharmaShell (2.6 + 1.7 + 2.8 SEK per share) provides support for a fair value of SEK 6.3-7.7 per share. Furthermore, we see that a successful start of clinical studies for both NEX-18 and NEX-20 can be expected to justify a revaluation to SEK 9 per share.

DISCLAIMER