Johan Widmark | 2025-02-20 08:00

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and Emergers is not subject to any prohibition on dealing ahead of the dissemination of investment research. This research does not constitute investment advice and is not a solicitation to buy shares. For more information, please refer to disclaimer.

Now targeting start of phase Ib/II before year-end

At the Q4 call, management stated that the extension of phase I for NEX-22, a once-monthly depot formulation of the GLP-1 analog liraglutide for type 2 diabetes, will not delay the development timeline, but that it will run alongside the other development efforts. Nonetheless, it now seems that the current target is to treat the first patient in the next phase Ib/II trial before year-end (as opposed to our previous expectation, in Q3’25). This trial will be a direct pharmacokinetic comparison of NEX-22 to Victoza, where Nanexa will focus on similarity in order to build on Victoza’s original documentation. If successful, a Pre-IND with the FDA could be held by the end of 2025. After completing Phase III with some 300-400 patients, an application for NEX-22 could realistically be submitted in 2028, with a product on the market by 2029, some three years ahead of any competing long-acting Semaglutide drug. This timeline presents a highly attractive opportunity for potential licensees of NEX-22.

Funding secured

With the directed issue of units in January amounting to SEK 35m, supplemented by SEK 20m in loans, Nanexa has now secured funding for its continued development activities into 2026. The loan includes an arrangement fee of 3% and carries an interest rate of 1% per month, while the directed issue resulted in a dilution of 13.5%, with an additional 15.9% dilution if the warrants are exercised (set at a subscription price of SEK 2.00 per share).

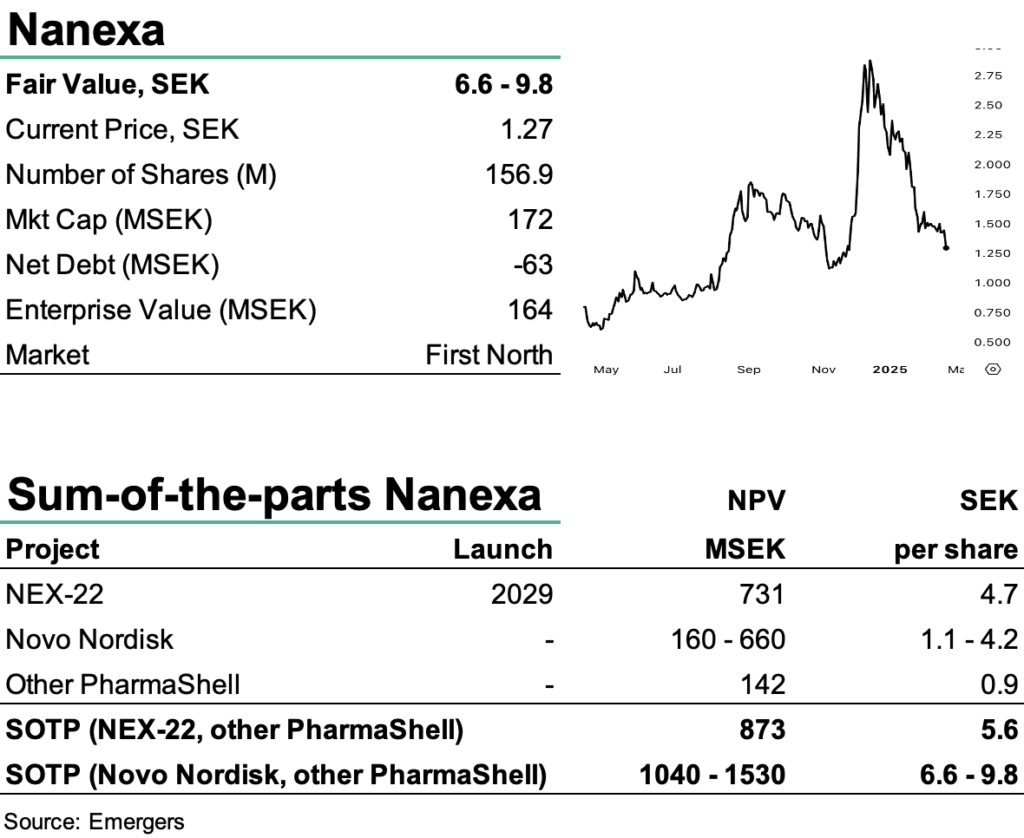

The recent positive results in the Phase I study have significantly improved Nanexa’s chances of securing a license deal, and Nanexa will now focus on the continued development of NEX-22 and the development project with Novo Nordisk, for which the company reports very promising progress. Adjusting for the dilution from the directed unit issue (but excluding the warrants), we now find support for an rNPV for NEX-22 alone of SEK 730m or SEK 4.7 per share. All in all, this means that we now find support for an rNPV of SEK 5.6-9.8 per share. However, we also note that, apart from securing a co-development license deal, there are not many catalysts for the share in the next 6-9 months.

DISCLAIMER