Johan Widmark | 2022-11-18 08:00

Adjustments stemming from Q2 weighing Q3

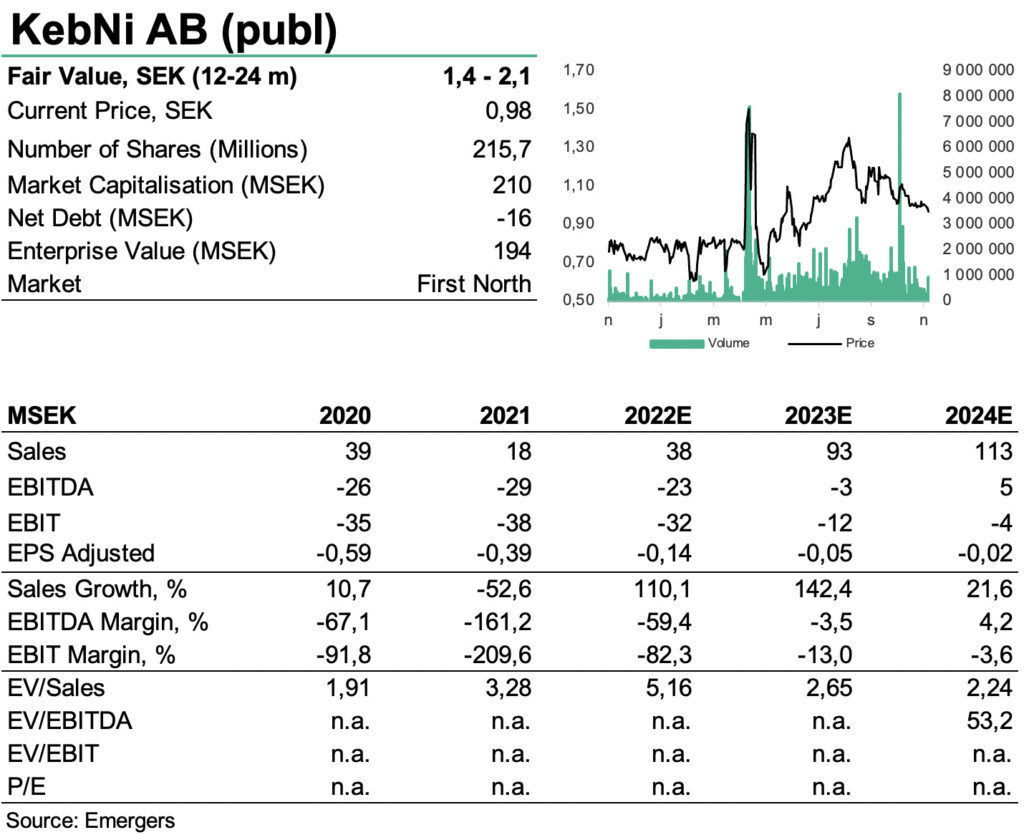

Top line sales in Q3 amounted to SEK 9.9m, but was affected by an adjustment from Q2 of SEK -2.3m resulting SEK 7.6m in reported revenues. Costs were also affected by SEK -3.4m from Q2. We have now adjusted our expectations for full year revenue to SEK 38 (46)m and expect a full year EBIT of -32 (-30)m.

Long term NLAW potential SEK 0,7 per share

With the SEK 76m volume order for IMUs from Saab placed in October, KebNi has now entered the next level of monetising its IMU technology. Work to increase capacity to series volume production is underway with deliveries scheduled to start in mid 2023 and last into 2024. By then we expect KebNi to have received follow-on orders. The first order received in October only scratches the surface of the potential with NLAW, as replacing only the units the UK has sent to Ukraine represent a potential for KebNi of over SEK 300m alone. Provided that KebNi receives follow-on orders we estimate that production at full capacity would correspond to revenues of around SEK 180m annually, after 2024. A rough assumption of a total of 25,000 new NLAW units over the coming 8 years, 50% gross margin and a discount factor of 20% would correspond to a NPV for just the ‘IMUs for NLAW’-business of SEK 0,7 per share. The volume component is however somewhat binary and not something we include fully in our forecast and valuation just yet.

New financial targets next catalyst for the share

We also continue to expect a pick-up in international orders in Satmission as well as other Inertial Sensing deals, and now expect a 20% growth rate for the non-Saab related business in 2023. Next major milestone is the announcement of KebNi’s revised financial targets later which we expect later in November. This will hopefully offer some welcome substance to our forecast for 2023 and beyond. All in all, our combined peer multiple and DCF-approach (WACC 20%) provide support for a fair value of SEK 1.4-2.1 per share in 12-24m with the upcoming announcement of new financial targets and follow-on orders from Saab as primary triggers.

DISCLAIMER