Johan Widmark | 2022-10-17 10:00

Long term NLAW potential SEK 0,7 per share

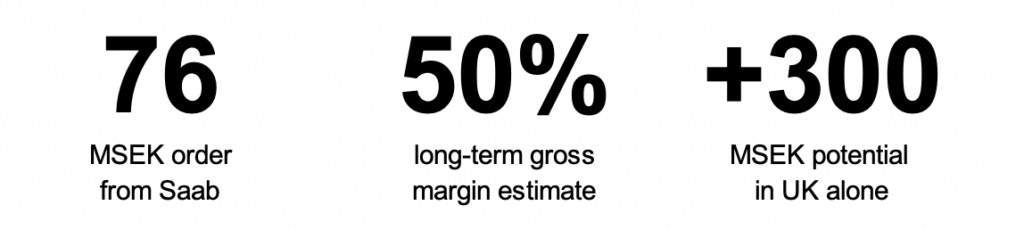

As we had expected, Saab has now submitted the first volume order for tailor-made Inertial Sensing units to be used in Saab’s single-use antitank weapon system NLAW, made famous for its role in fending off Russian tanks in the war in Ukraine. Deliveries are planned to start in mid 2023 and last into 2024, after series volume production preparations have been finalized. The weapon has been in use since 2009, with a total of over 24,000 units produced, of which 10,000 has been gifted to Ukraine.

A simple calculation shows that if the UK were to replenish its stocks after the units sent to Ukraine, this would mean a business potential of SEK 300-400m for KebNi, to the UK alone. But considering the impact NLAW has had in Ukraine, the demand for NLAW can be expected to increase significantly from many other countries. This means that the SEK 76m order is most likely only the first of many to come for a long time ahead. Provided that KebNi receives follow-on orders we estimate that production at full capacity would correspond to revenues of around SEK 180m annually, which means we expect the bulk of the NLAW volume production to occur beyond our forecast horizon in 2024.

A rough assumption of a total of 25,000 new NLAW units over the coming 8 years, 50% gross margin and a discount factor of 20% would correspond to a NPV for just the ‘IMUs for NLAW’-business of SEK 0,7 per share. The volume component is however somewhat binary and not something we include fully in our forecast and valuation just yet.

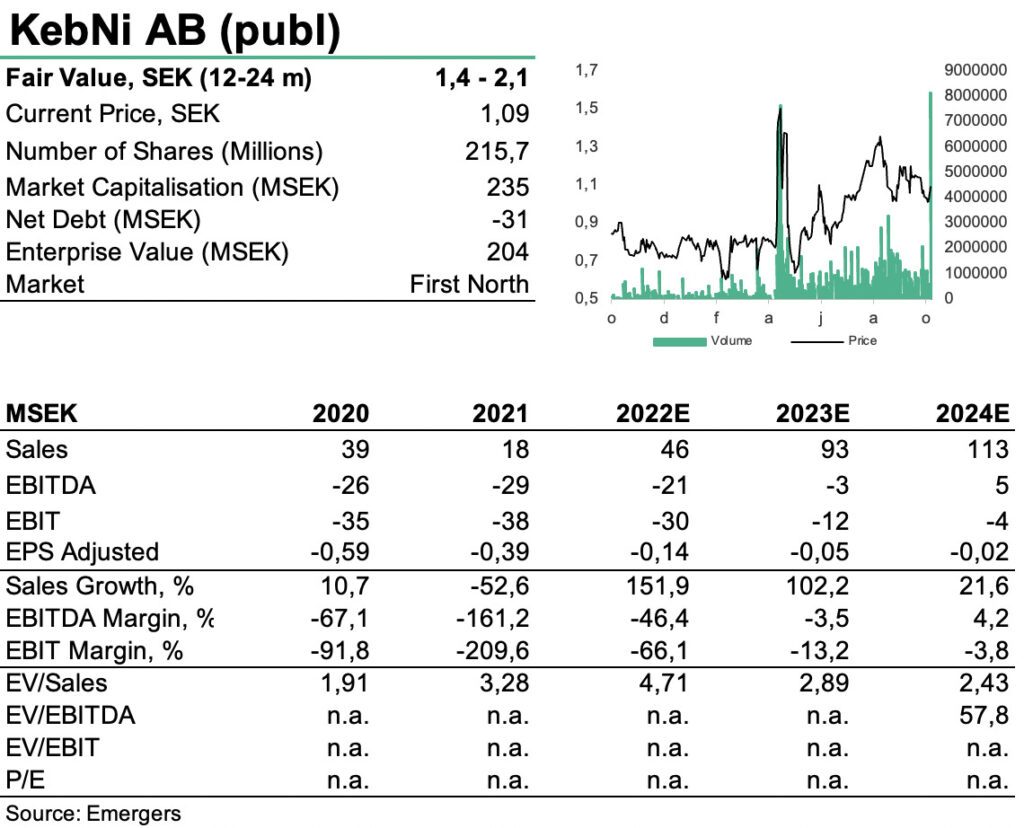

Lower risk but higher general risk premium

In addition to the Saab order, we continue to expect a pick-up in international orders in Satmission as well as other Inertial Sensing deals. Also, the bankruptcy of local peer Datapath in May this year gave KebNi the opportunity to add personnel with relevant experience. All in all, we continue to expect a pick-up in revenues in H2’22 and maintain our full year forecast at SEK 46m for 2022. We also raise our revenue forecast for 2023, from SEK 83m to SEK 93m, which implies a 20% growth for the non-Saab related business in 2023.With the series production order we now look forward to the announcement of KebNi’s revised financial targets later in Q4’22, which hopefully offers some welcome substance to our forecast for 2023 and beyond. Following the Saab order, our forecast adjustments and a general expansion of the risk premium in the market (WACC 20%), we now find support for a fair value of 1.4-2.1 (1.2-1.8) per share in 12-24m and see the upcoming announcement of new financial targets and follow-on orders from Saab as primary triggers.

DISCLAIMER