Johan Widmark | 2022-08-30 11:30

High activity converting to revenues in H2 and beyond

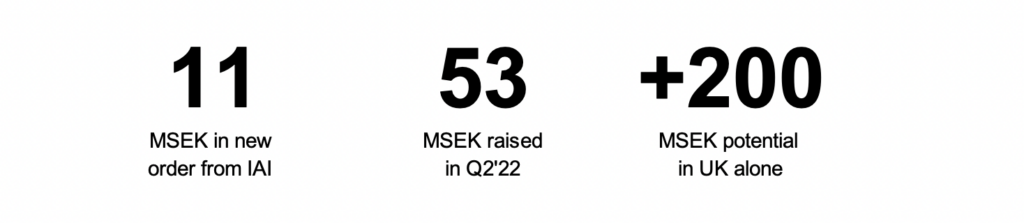

Sales came in at SEK 7.2m in Q2’22, while costs increased somewhat in line with the accelerated development and preparations for, and investments in, volume series production capability of the IMUs for SAAB’s NLAW. For the second half of 2022, we expect a pick-up in international orders in Satmission as well as continued deals in Inertial Sensing. Guided by the good momentum across all KebNi’s business areas we are confident about a pick-up in revenues in H2’22 and maintain our full year forecast at SEK 46m for 2022.

IMUs for NLAW key piece of the puzzle

Considering the pivotal role NLAW has played so far in Ukraine, the demand for NLAW can be expected to increase significantly from other countries in Russia’s vicinity. The NLAW is almost unique with the exception of one comparable competitor, the American Javelin, which is about 6x as expensive. A simple calculation shows that if the UK were to replenish its stocks after the 10,000 NLAW it sent to Ukraine and we assume a price per IMU at the lower end of the range for the variety used in NLAW, this would mean a business potential of SEK 200-300m for KebNi, to the UK alone. The time horizon and scope of such series production orders are still unclear, but we note the supplementary order from SAAB regarding NLAW in mid-March this year which indicates that bigger things are afoot.

This kind of series production orders are most likely an integral piece for the management in constructing KebNi’s revised financial targets. Delivery phase can be initiated after series volume production preparations have been finalized in H2 2023, but the first order would need to be placed well ahead of that, especially in light of the global component shortage and pressured supply chains. While the new targets will be announced in the autumn, it is more uncertain when the first order for serial production may come, but we expect this autumn too. Together these constitute the two most important triggers both for the share and for understanding what the future KebNi will look like.

Further upside potential once key triggers kick in

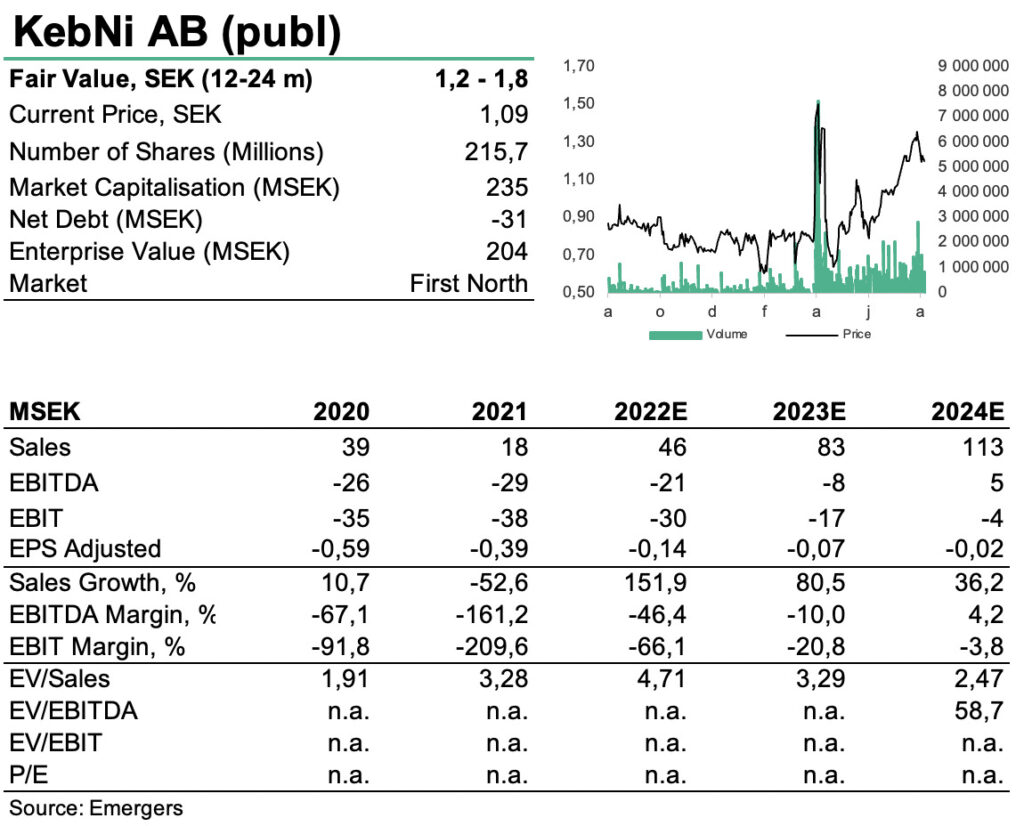

Until we get a better picture of the magnitude of the series volume orders, it is hard to estimate the pace of a future volume ramp-up, other than that we’re likely to see heavier investments in production in the near term in order to capture higher volumes down the road. Until then, we expect the main impact from NLAW volume production to occur beyond our forecast horizon in 2024, meaning that we keep our topline forecast in 2022-2024 unchanged. After a doubling in the share price since spring, KebNi is now close to the low end of our fair value range of SEK 1.2-1.8 per share in 12-24 months, with a significant further upside potential once the two aforementioned key triggers kick in.

DISCLAIMER