Johan Widmark | 2022-02-28 08:00

Final delivery to IAI delayed until Q1 2022

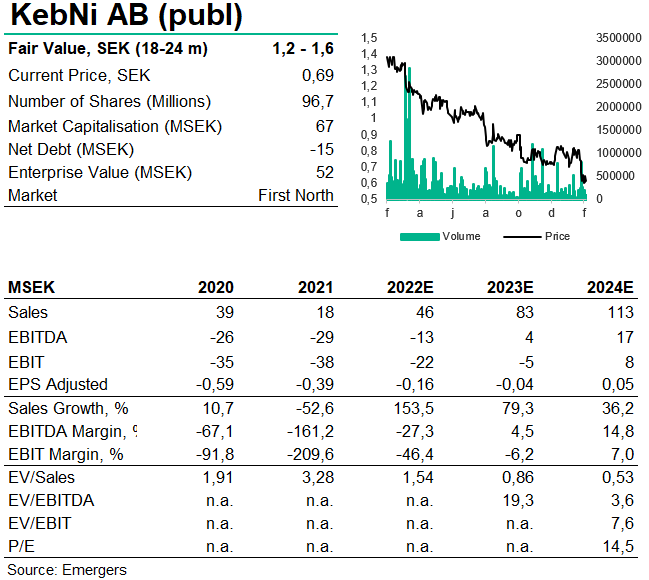

The report for the fourth quarter showed continued recovery compared with the weak start to the year in terms of sales, with full-year sales of SEK 18m, just under our SEK 21m forecast. This is lower than our original forecast since the final delivery to IAI has been postponed until Q1 2022. In terms of activity, the fourth quarter of 2021 included a number of points that support the company’s strategic plan for 2022-2026. For example, Satmission’s framework agreement for Drive Away antennas to Turkey made a surprisingly strong start, with three orders totalling SEK5m. For the IMU work on Saab’s NLAW portable anti-tank weapon, the company says that the invasion of Ukraine (where pictures are currently being spread on social media of a burning Russian tank that is said to have been hit with an NLAW that Ukraine received via the British) could mean a shortened schedule if increased demand brings forward Saab’s requirements.

Increased business activity and reach

The sales organization has increased from 1.4 to 4 individuals, and KebNi has increased its international representation from one to 17 countries. Together with a number of existing business opportunities and ongoing discussions in maritime satellites, the new SensAItion IMU family, and an opportunity to introduce the company’s upcoming position monitoring application in South Korea, this provides support for a major boost in business activity in 2022 and 2023. At the same time, we note that the European Commission in February this year launched a new EUR 6 billion satellite communications plan to reduce the EU’s dependence on non-EU companies and address the increased satellite activity of Russia and China. Overall, this provides support for KebNi’s strategic plan for 2022-2026, to grow SatCom at a pace above market growth and match Inertial Sensing in size by 2025, show positive operating profit by H2 2023, and positive cash flow by 2024.

Support for high revaluation potential to SEK 1.2−1.6

After the final delivery to IAI during Q1 2022, we expect that the company’s IMU efforts and increased market activity within SatCom will start to bear fruit in 2022, and we maintain our forecast of a sharp increase in sales this year and next year to SEK 46m and SEK 83m, respectively. This rhymes with the company’s goal of showing a positive operating profit by H2 2023. We have previously highlighted KebNi’s need to strengthen its cash reserves, as the bridging loan of SEK12m and the cash of SEK 15m cannot be expected to suffice until cash flow is positive. A new rights issue of SEK 20m at today’s squeezed share price would mean dilution of around 35%. With accelerating momentum in activity and development efforts, and good prospects for payback in 2022 and 2023, we see support for a fair value based on DCF and comparison multiples of SEK 1.2-1.6 (1.2-1.8) per share on a horizon of 18-24 months.

Read Emergers’ report on kebNi here

DISCLAIMER