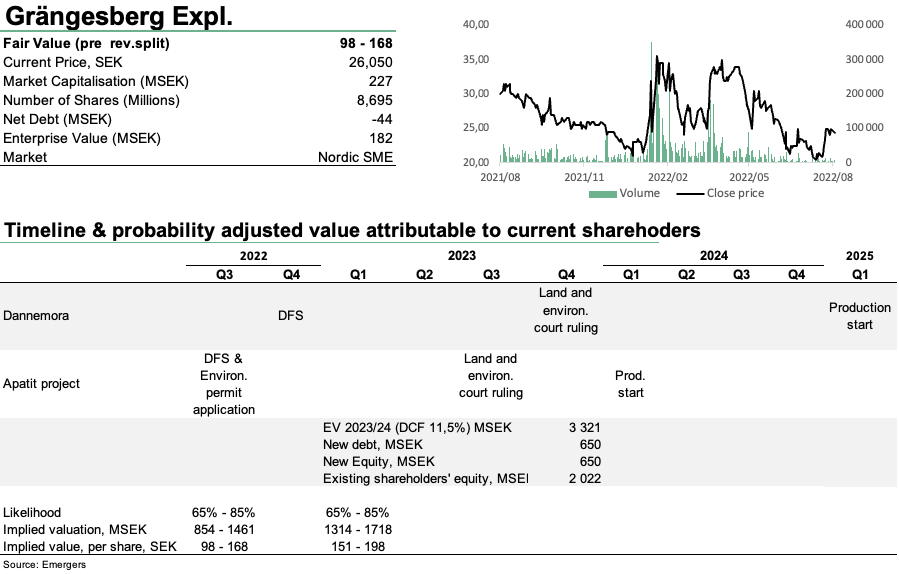

As a result of the ongoing preparations of the DFS for Dannemora, GRANGEX now reports an upwards revision of the known and indicated mineral resources, following a reinterpretation of the drill cores, by 990 kT to 29,176 kT. Inferred resources are also increased by 125 kT of 36.6% iron. While this signals strength with regards to cost efficient project development and how modern mining methods can add value to old projects, it has marginal effect on our fair value, where we now find support for SEK 98-168 (95-163) per share in 12-24 months. However, with a structural long-term growth in demand for green CO2 free iron ore and a prolonged supply crisis following Russia’s cut off from Europe, macro developments continue to benefit both of GRANGEX’s projects, which along with continued operational progress should benefit a revaluation of the share.

Johan Widmark | 2022-08-10 08:00

Next step DFS for Apatite in Q3 and Dannemora in Q4

In the very last days of Q2’22, after some minor delays, GRANGEX submitted the environmental permit application to the Swedish Land and Environmental court for the restart of Dannemora to produce high grade iron ore. Now the next step is to finalize the Definitive Feasibility Study (DFS) for Dannemora which we expect before the year end. In total there are 18,000 meters of drill cores that have been tested, accounting for about 50% of the relevant cores, meaning that there are more cores to test, which could changes resource estimates, and our fair value, further.

With regards to the Apatite project we expect the submission of the environmental permit application already in Q3’22 along with the DFS. With the major financing round for these projects most likely during H1’23, we maintain our projection of production start for the Apatite project around winter ‘23/24 and production start in Dannemora around winter ‘24/25.

War in Ukraine continue to offer support to prices

Iron Ore prices have seen a slight pullback from the levels seen after Russia invaded Ukraine, but remain at 130+ USD per ton. Historically, Russia has accounted for over 20% of European imports of high grade iron ore and pellets, and with no quick solution in sight, this continues to lend support to our expectation of a continued expansion of the price premium for higher grades, such as the best in class 68% quality to be produced at Dannemora.

The war in Ukraine and subsequent trade restrictions have also continued to push prices of phosphate rock further, where prices have surged to now being closer to 300 USD/t. To be prudent, we include only a small portion of these price changes into our valuation model, but note that they provide a bright backdrop for the projects which enhances GRANGX’s chances to finance the projects at attractive levels in H1’23 as well as the chances to potentially include some form of trade financing into the mix.

Significant upside based on risk adjusted DCF

While risk appetite has recovered slightly in July/August, we maintain our key model assumptions for both projects, which show a very healthy financial profile, with a NPV at SEK 3.3bn and a repayment within three years. Reduced by project financing for both the Apatite project and Dannemora, where we expect debt of SEK 650m and new equity of SEK 650m, approximately SEK 2bn remains attributable to today’s shareholders. With an estimated probability of successfully passing the next two years’ milestones of 65-85% per year, this provides support for a fair value today of around SEK 850-1,460m or SEK 98-168 per share.

Should the management decide to include a trade finance solution into the financing mix, this would probably cap some of the upside with regards to rising iron ore and/or phosphate rock prices, but also limit shareholder dilution and raise potential further.

DISCLAIMER