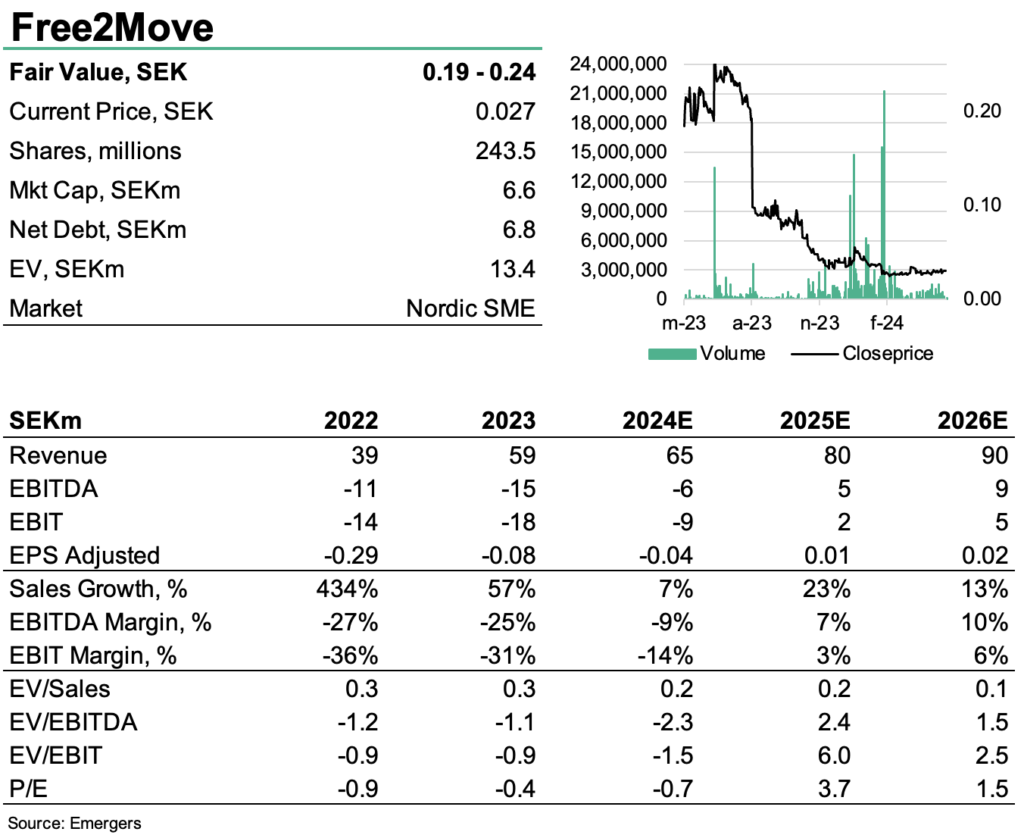

Somewhat surprising, the QoQ reduction in order backlog from SEK 23m in Q4’23 to SEK 15m in Q1’24 was less than revenues of SEK 6.3m in the quarter, suggesting that F2M has seen some cancellations. That should however have improved after Q1 with 34% order intake growth in April, when three out of four subsidiaries reported positive operative results. A SEK 8.4m working capital release helped CF to a mere SEK -0.9m, but liquidity continues to be a glaring risk. Should the company manage to secure the necessary financial leeway, we expect it to reach profit in 2025, which should drive a revaluation of the depressed share price, now trading at EV/Sales 0.2x ‘24e and EV/EBITDA 2.6x ‘25e. All in all, we now find support for a fair value of SEK 0.15-0.20 (0.19-0.24) per share, provided that a rights issue can be avoided.

Johan Widmark | 2024-05-16 08:00

Weak Start – Improved Cash Flow

Free2Move had a slow start to 2024 due to adverse weather and the aftermath of negative financial and media sentiment, which dampened investment enthusiasm. However, in March, the subsidiaries saw stronger results and significantly improved cash flow compared to the same period in 2023, nearing positive figures. Subsidiaries Solortus, Sydvent, and the 2Connect platform have continued to shift focus from product development to services for customers interested in sustainable solutions, as the underlying demand for smart and sustainable property management is higher than ever. Subscription services, particularly in energy storage through ’Statera,’ increased by 38% compared to the previous year, indicating a positive trend. Furthermore, Free2Move’s market expansion, especially in Copenhagen, grew by 59%

Focus on profitability but liquidity a bottle neck

Sales in Q1’24 came in at SEK 6.3m, compared to SEK 14m same period last year, while EBIT was SEK -8.5m compared to SEK -3.1m in Q1’23. Op CF was not as weak, at SEK -0.3m. Cost-savings and consolidation efforts are planned to be completed in Q3’24, which is expected to further improve our operational efficiency and profitability, with a full cost-reduction effect of 10% from Q1’25. With Energy savings of 43% for customers, corresponding to a total energy savings of 75 million kWh, F2M continues to expand installed base, now at nearly 800 installations.

Depressed share price creates long term opportunities

Despite the historic downward pressure on the share, we see a considerable upside potential in the F2M share. This hinges on the company reaching neutral cash flow and profit in 2024/2025. With the measures taken to more effectively work the order backlog, continue growth and raise profitability, the outlook for this is bright. Follwing the weak start to the year, we have revised our sales forecast and now find support for a fair value of SEK 0.15-0.20 (0.19-0.24) per share, provided a rights issue can be avoided.

DISCLAIMER