Written by johan@emergers.se• 2024-03-27•

12:00•

Analys, Research

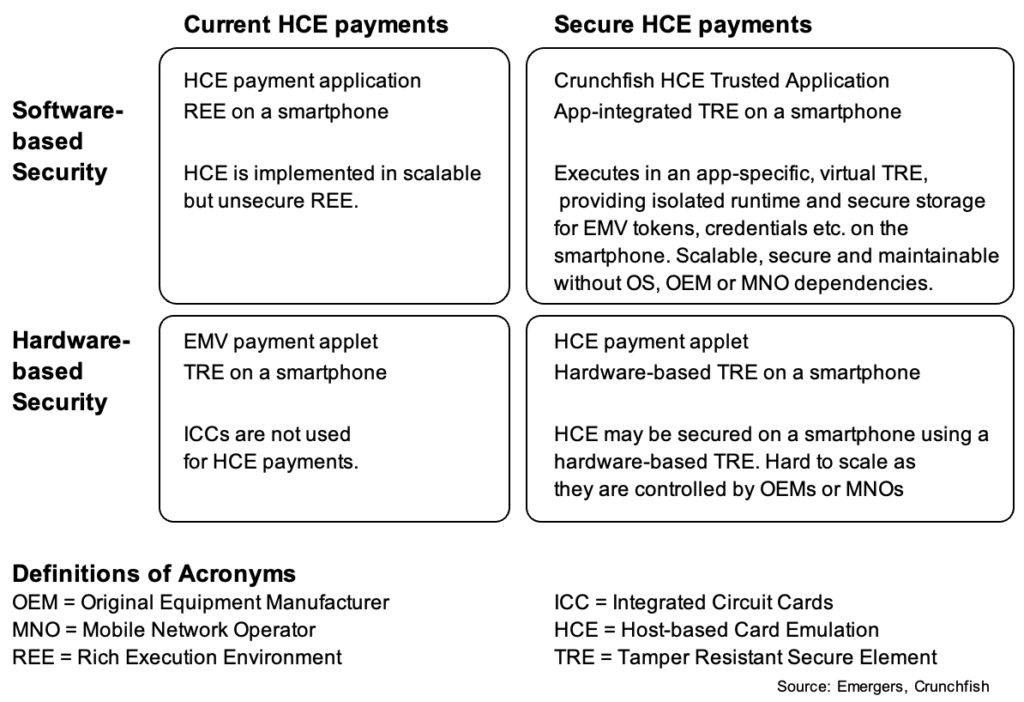

CRUNCHFISH: Major TAM expansion with broadening to secure and scalable mobile card payments

HomeAnalys, ResearchCRUNCHFISH: Major TAM expansion with broadening to secure and scalable mobile card payments

2025-04-01•

Analys, Research

Following the many recent grants, notices of allowance and intention to grant patents in Europe and the US, and the arrival of the first of...

Read More →

2025-03-10•

Research

Johan Widmark | 2025-03-10 10:30 Read the report in PDF here With production now commenced at the 110MW Waste to Energy (WtE) plant in...

Read More →

2025-02-14•

Analys, Research

Johan Widmark | 2025-02-14 08:00 READ FULL REPORT IN PDF HERE Small signs pointing towards a system-wide deal in India At the...

Read More →

2025-01-24•

Analys, Research

With the release of a Preliminary Economic Assessment (PEA) for the restart of the Sydvaranger mine, GRANGEX now has more clarity on the...

Read More →