Johan Widmark | 2024-06-19 08:00

Building a solid platform for expansion

With the recent announcement that Cindrigo has exited the Slatina 3 geothermal project in Croatia, citing better investment stability and value in Germany, the Company has strategically realigned its portfolio to focus on high-value, lower-risk renewable energy projects across Europe. By prioritizing the 110 MW Waste to Energy plant in Finland and three geothermal projects in Germany, Cindrigo aims to harness immediate revenue potential and scalable growth opportunities.

Kaipola set to generate first revenues in Q4’24

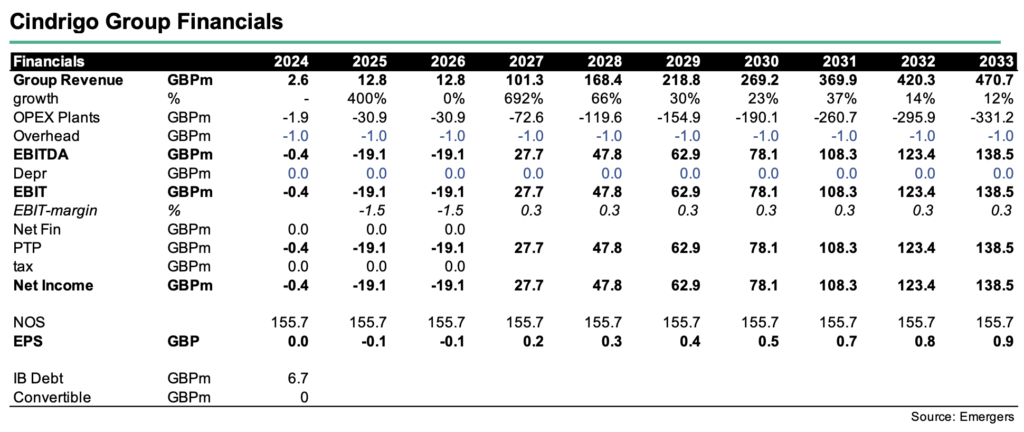

Having closed the acquisition in Finland means Cindrigo has now secured a significant foothold with a 50-year lease on a 110 MW Waste to Energy (WTE) combined heat and power (CHP) plant in Kaipola. With the plant already built, currently undergoing maintenance and upgrades, this will offer revenues already in Q4’2024, with a projection to generate EUR 15 million in its first year of operation, and annual revenues of EUR 40m at full capacity, then contributing EUR 10m in EBITDA.

Remarkable government support for geothermal production

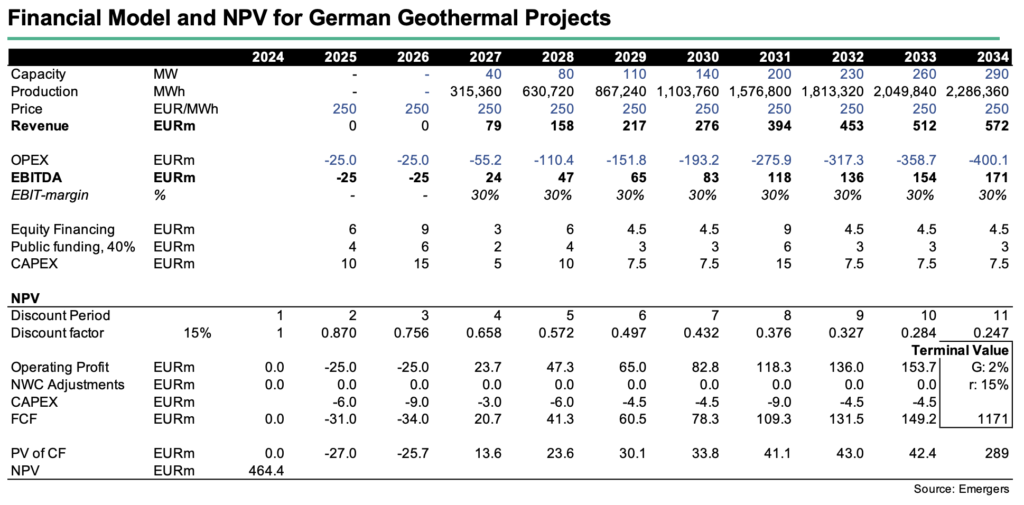

In April, Cindrigo announced the signing of a term sheet with Zukunft Geowärme GmbH to acquire three geothermal energy projects in the Upper Rhine Valley. With an initial target capacity of 80 MW, and a significant expansion potential exceeding 300 MW combined geothermal power and heat, this will give Cindrigo a ca 200MW under contract proving a strong platform for further expansion. Importantly, Germany offers strong government support for geothermal projects with substantial incentives, including a feed-in tariff of EUR 250 / MWh for 20 years and up to 40% federal funding for construction CAPEX. A federal insurance policy is also underway which will essentially eradicate all explorative geothermal drilling risk. This robust support framework positions Cindrigo well to capitalize on Germany’s ambitious target to increase its geothermal heating capacity by 2030.

With the German projects expected to begin generating revenue by Q3/Q4 2027, our NPV shows an Unlevered NPV (15%) of EUR 460m. This however does not take financing or the acquisition cost, which is still undisclosed, into account, and runs a high risk of requiring additional funding to reach its full production potential.

Most but not all pieces in place for a transparent valuation of long-term potential

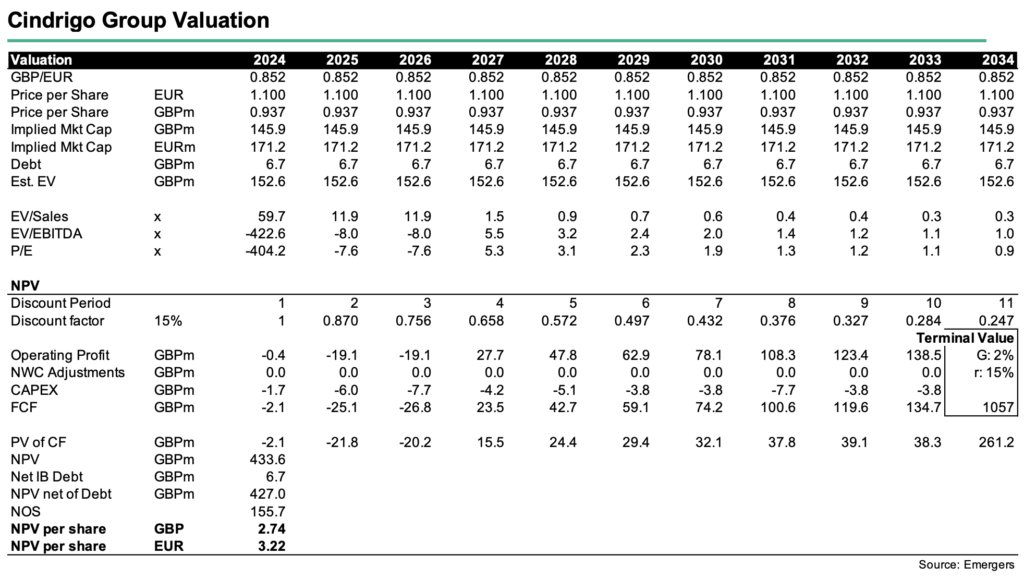

Before any new listing, the most recent data point on valuation is the EUR 1.1 per share at which the payment in shares for Kaipola was made. This implies a Market Cap of GBP 146m / EUR 171m.

Scaling the capacity in Finland and Germany at a linear CAPEX / Production ration and a 15% WACC supports a NPV for the group of GBP 434m. At 155.7m shares after the Kaipola acquisition, this translates to GBP 2.74 / EUR 3.22 per share. This number however needs to be adjusted with the acquisition price for the projects in Germany, which is still undisclosed but should till leave plenty of upside potential in the valuation.

To materialize the Company’s long-term target of 1,000MW we believe that additional external financing will be needed, diluting the Cindrigo shareholders further. The dilution is dependent on how successful the initial rollout is, and how much can be re-invested into new plants.

In our view, the investment case of Cindrigo boils down to how quick, and at what terms new capital can be raised to finance the rollout. Since the company is pursuing a somewhat untouched market with huge growth opportunities, and is run by a management with proven track record, almost all the pieces are in in place for success.

DISCLAIMER