With a prolonged Russian cut-off from Europe, Russia’s energy war against the natural gas-dependent continental Europe has put self-sufficiency of sustainable energy at the top of the agenda. Cindrigo is now in the starting blocks of a geothermal power multi-plant rollout, starting with 20MW in Croatia operational in 2024, to produce a total of +150 MW of clean baseload power by 2026. We now find support for a risk-adjusted fair value range of GBP 1.00-1.20 per share, solely based on the Croatia projects, noting that a successful rollout should elevate the fair value to roughly GBP 2.00 per share in 2024, and where the company’s plan for a broader rollout could lift Cindrigo into a multi-billion GBP-company.

Andreas Eriksson | 2023-04-06 20:00

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and Emergers is not subject to any prohibition on dealing ahead of the dissemination of investment research. This research does not constitute investment advice and is not a solicitation to buy shares. For more information, please refer to disclaimer.

Macro trends pave the way for clean baseload power

Decreasing deliveries of Russian natural gas combined with rising inflation and interest rates have put the European energy market under pressure. The demand for baseload power is high, and geothermal power is one of few renewable baseload power sources, next to bio- and hydropower. Geothermal can be used anywhere, but due to differences in topography, some geographic areas are better suited than others. Despite the current financial climate, renewable energy companies have been solid, and seen as safe haven by investors. One example is NYSE listed Ormat Technologies, currently trading at 36x EBITDA.Large portfolio of renewable energy projects

Through the acquisition of Energy Co-Invest Global (ECG), Cindrigo gets access to a large portfolio of renewable energy projects at various stages of development. The initial focus will be in Croatia, where Cindrigo has a license to construct a 20MW geothermal power plant (Slatina 3), but where the company sees a high probability to add additional licensing blocks of up to a total of 100MW at the 57 sq.km. site alone. With the ECG-portfolio, Cindrigo also sees plenty of opportunities for further expansion into Croatia, Serbia, Hungary, and Romania. Despite current market conditions, Cindrigo has managed to sign a USD 75m Finance Framework Agreement with Abu Dhabi based Petroline Energy, where Petroline will invest an initial GBP 23m into Slatina 3 through a 10-year convertible note at 6.5% per year. Cindrigo has also secured a Framework Agreement with geothermal industrial giant Kaishan, regarding an EPC- and O&M contract for Slatina 3, including financing of 70%.Unlocking potential with focus on proximate cash flows

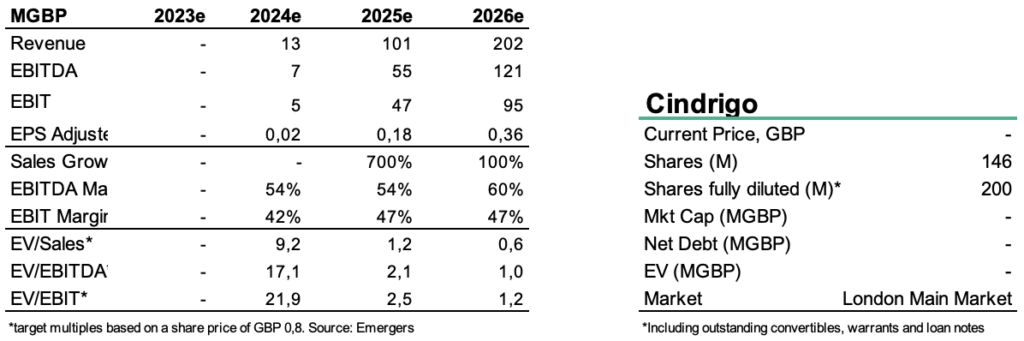

We see the rollout in Croatia as the fundamental core of our valuation of Cindrigo and the base for our DCF and peer multiple approach, and consider the remainder of the ECG project portfolio as high-value options. With a gradual rollout, with securing project financing as a first step, constructing the first 20 MW plant by 2024 to reach +150 MW by 2026 we find support for a fair value range of GBP 1.00-1.20 per share in 12-24 months (including estimated accumulated debt and dilution effect from new equity), while a succesful multi-plant rollout indicates a significantly higher upside. The upcoming listing on London Main Market will be an important step as it can provide easier access to external capital (each plant will be run in its own SPV with external funding required for each plant), at least until internally generated cash flows can be re-invested. In light of the recent discussions with suitable partners and the low risk nature of geothermal power contracts, we remain optimistic about the company’s long-term rollout plan.

DISCLAIMER