Johan Widmark | 2025-03-10 10:30

With production now commenced at the 110MW Waste to Energy (WtE) plant in Finland, generating its first, albeit modest, cash flows, and the now finalized strategic expansion into high-value geothermal projects in Germany, Cindrigo is on track to position itself as one of the most interesting renewable energy developers in Europe. Despite the 37% dilution resulting from the deep discount offered to existing shareholders in the GBP 13 million capital raise, the company is now close to being debt-free. The planned listing on the LSE Main Market in H1 2025 under the Commercial Companies category will bring added benefits, including increased scrutiny, transparency, and eligibility for institutional investments and index inclusion, potentially elevating the company to a new valuation bracket.

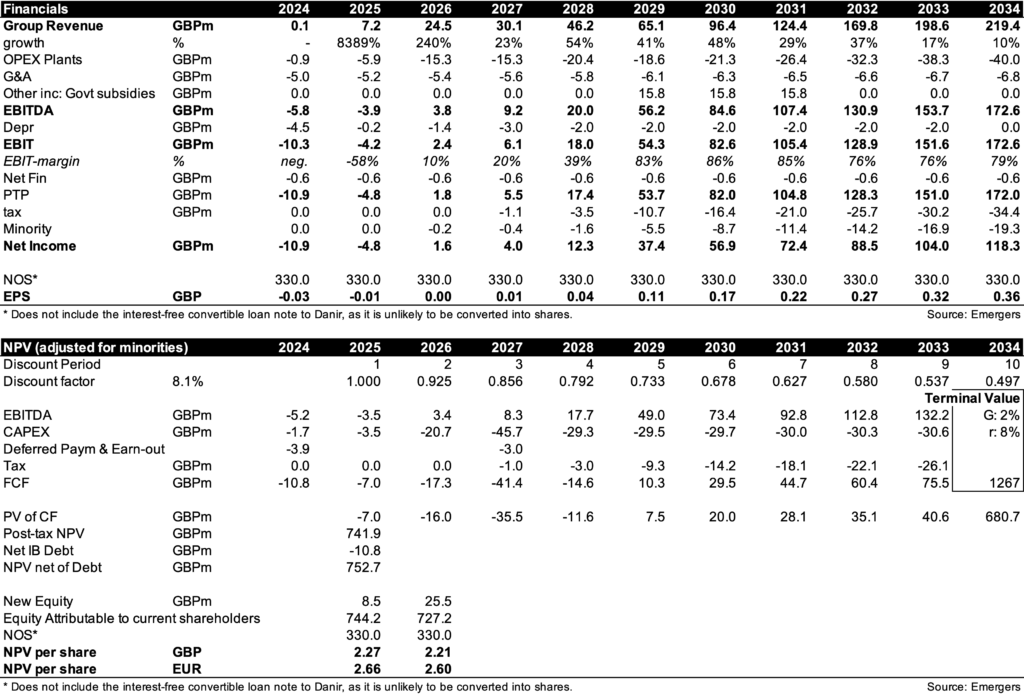

Operationally, our revised forecast for the 110MW Kaipola WtE plant now includes the option to incorporate commercial waste into the fuel mix, supporting an annualised EBITDA of EUR 15 million by 2027 and a run-rate of EUR +30 million by 2029, although this final increase will be associated with a EUR 20 million investment. This cash flow, combined with robust support for the German geothermal portfolio—including government grants, EUR 250/MWh feed-in tariffs, and financing from the Kaishan Group—establishes a stable financial platform for future project development and enhanced support for future long-term debt financing.

The recent completion of the acquisition of the German assets, with an option to increase Cindrigo’s ownership with 5% from 85% to 90% in 2026, with 80MW capacity in the initial phase and a total potential exceeding 300MW, position Cindrigo to capitalise on Europe’s high energy prices, decarbonisation requirements, and focus on energy security. Factoring in a EUR 20m EBITDA contribution from Lithium production by 2030, we see potential for a group EBITDA of EUR 100m (GBP 85m) that year.

With initial cash flows and financing effectively lowering risk, we have adjusted the WACC to 8.1% (previously 9%) and now find support for a fair value of GBP 2.21–2.27 per share on a 12 month horizon, although some discount is motivated during the scale-up on Finland. Applying a peer-level 15x EBITDA multiple to our 2030 forecast (adjusting for the EUR 19m government subsidy and minorities) suggests an upside potential to a market capitalization of around GBP 900m, equivalent to GBP 2.6–2.8 per share. In a longer perspective, to 2034, we find that the further growth and profitability measures support a share price in the GBP 5-10 per share range.

DISCLAIMER