Johan Widmark | 2024-05-15 10:00

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and Emergers is not subject to any prohibition on dealing ahead of the dissemination of investment research. This research does not constitute investment advice and is not a solicitation to buy shares. For more information, please refer to disclaimer.

Continued adverse impact from plant disease in Q1

Revenue in Q1’24 was the company’s second highest for a first quarter, amounting to SEK 7.3m (SEK 11.3m). Agtira’s largest facility, Härnösand, had a low capacity utilization of 59% compared to 76% in Q1 2023 due to a plant disease previously communicated. The measures Agtira took to improve cultivation and increase resilience had a positive effect, and company reports that a positive trend was noted at the end of Q1 with the highest productivity ever in a single greenhouse. EBIT in Q1 was SEK -10.6m.

Several significant launches pointing to SEK 100m in ARR

In Q1, Agtira signed a 10-year agreement with the food chain Lidl Sweden, meaning that Agtira will deliver cucumbers to all 200+ Lidl stores in Sweden. Through the Farming-as-a-Service model, Agtira will build and operate a production facility of approximately 10,000 square meters. With an estimated SEK 4m in annual sales per 1,000 sqm this gives a total contract value of SEK 400m over 10 years. Additionally, we now continue to look forward to the establishment of three new production facilities, the ICA Maxi in Haninge, the Greenfood system in Boden, and the Coop Nord system in Umeå. When these are completed we estimate a total annual recurring revenue (ARR) of SEK 97m.

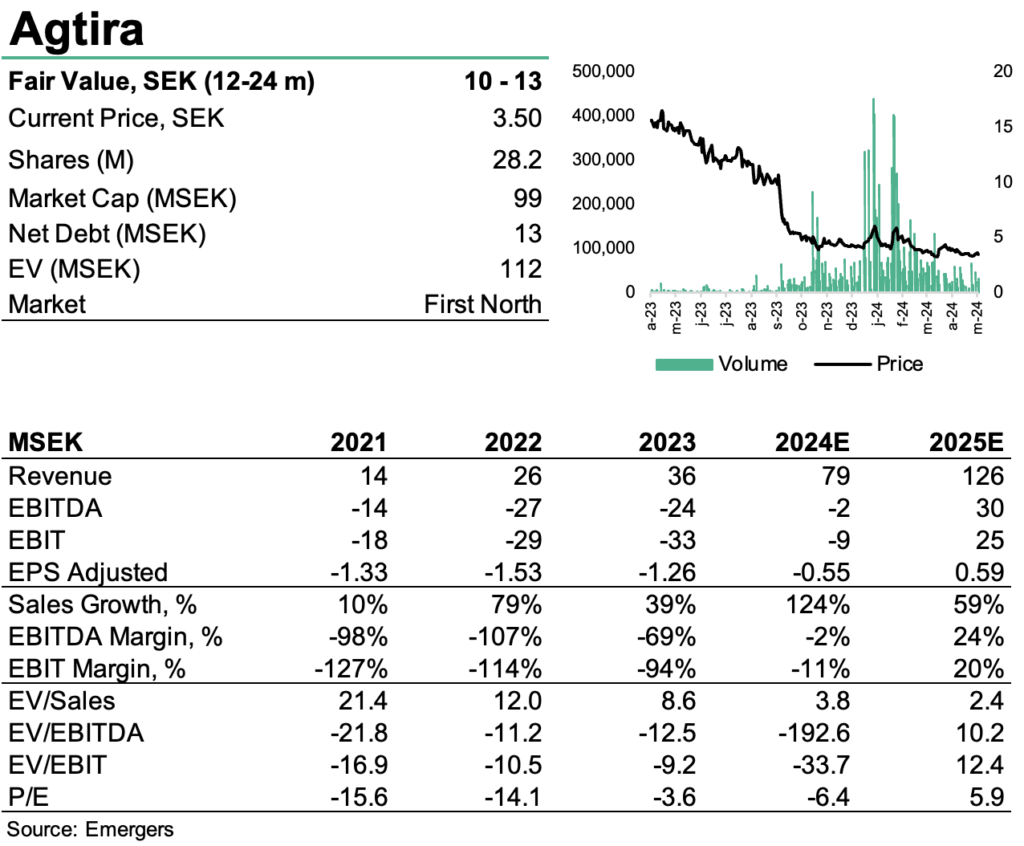

Fair Value of SEK 10-13 provided a rights issue can be avoided

Following the rights issue concluded in Q4’23, we estimated that the SEK 47m net raised meant that operation would be financed until positive cash flow can be reached. In Q1’24 however, Op CF of SEK 12m and investment of SEK 20m pushed Net CF to SEK -32m, leaving liquidity at SEK 15m. We thus note an elevated pressure on the company to strengthen finances through working capital release and increased revenues, which is our main scenario . But a rights issue to fund the forthcoming scale-up cannot be ruled out. All in all, Agtira is poised to make 2024 the year where the growth story truly takes off and we now find support for a fair value range of SEK 10-13 (14-16) per share.

DISCLAIMER