Andreas Eriksson | 2023-02-15 12:00

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and Emergers is not subject to any prohibition on dealing ahead of the dissemination of investment research. This research does not constitute investment advice and is not a solicitation to buy shares. For more information, please refer to disclaimer.

Solid foundation for continued growth

While full year sales for 2022 came in at a strong 25.5 MSEK, an 80% increase from previous year, costs increased at a similar pace, mostly driven by high energy prices at the facility in Härnösand. We’re not too concerned about this, and see the three systems, a number of LOI:s and the traction for the company’s FaaS-model as the key takeaways from 2022. We’re still waiting for more information regarding the big Greens-system, planned in connection to ICA Maxi Haninge, and the simultaneous construction of Greenfood’s first system. In addition, Agtira also has ongoing LOI:s with Coop Nord, Beehive Blockchain and Norwegian Minnesund Näringspark, totalling the number of systems operational, under construction or under LOI to 17 systems.

Deepened relationship with Greenfood

Agtira’s relationship with Greenfood has deepened, as the international giant now will bear all costs for production of cucumbers in Agtira’s own R&D-center in Härnösand, while the two parties share all profits from it. This deal the company estimates to be worth around 100 MSEK over three years. We believe this kind of relationship, with a bigger partner with international reach, might be exactly what Agtira needs for an expansion to continental Europe as well as over the Atlantic and potentially also to the Middle East in the longer run. Further details regarding either an even deeper relationship (we deem Greenfood a potential financing partner for new systems) or new firm deals will lower the risk of the investment case.

Liquidity the main bottleneck to unleash full potential

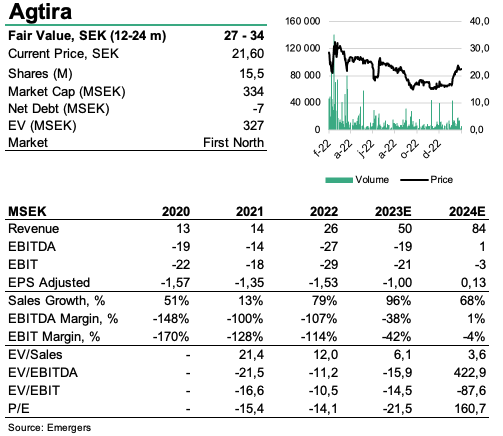

All in all, Agtira has over the year proven there’s a demand for all of their three systems, Complete, Greens and InStore. And with another 14 waiting to be constructed or under LOI we expect a positive news flow in the upcoming months. The new deal with Greenfood supports an adjustment of our forecast where a total of 17 systems installed by 2024 will generate 84 MSEK in recurring revenue which in our combined DCF- and target multiple approach support a fair value of 27–34 SEK per share, in 12-24 months. Liquidity continues to be the main bottleneck, dampening a quicker rollout as the bigger systems ties a lot of capital. Should Agtira find a solution to this, a more rapid rollout will drive a re-evaluation of the share, while an international expansion would add even more to the upside potential.

DISCLAIMER