Johan Widmark | 2025-04-01 08:00

Positive pre-clinical data

The pre-clinical data of clinical sensitivity and specificity were estimated from 94 chest-pain samples (46 with confirmed myocardial infarction) measured on in-house prototype instruments and also measured on Psyros™ commercial prototypes. The areas under the ROC curve (AUC) were 0.97 and 0.98 respectively, demonstrating good clinical performance. The correlation between in-house laboratory prototypes and commercial prototypes (R²) of 0.97 confirms that Prolight’s low-cost optical module can deliver the performance required for launch. These first results, will be instrumental in fine-tuning and final optimisation of the Psyros POC system, mitigating risks, and ensuring the robustness of the final design before going into the full clinical performance study planned to start later in 2025, with commercial launch in 2026. The positive results from the pre-clinical validation study de-risk the full clinical validation of the Psyros high sensitivity troponin assay. These results combined with the portable commercial Psyros prototype with low cost optical module motivate a hike of the likelihood to launch to 90% (82%).

Cash now at SEK 15.7m excluding grants and R&D tax credit

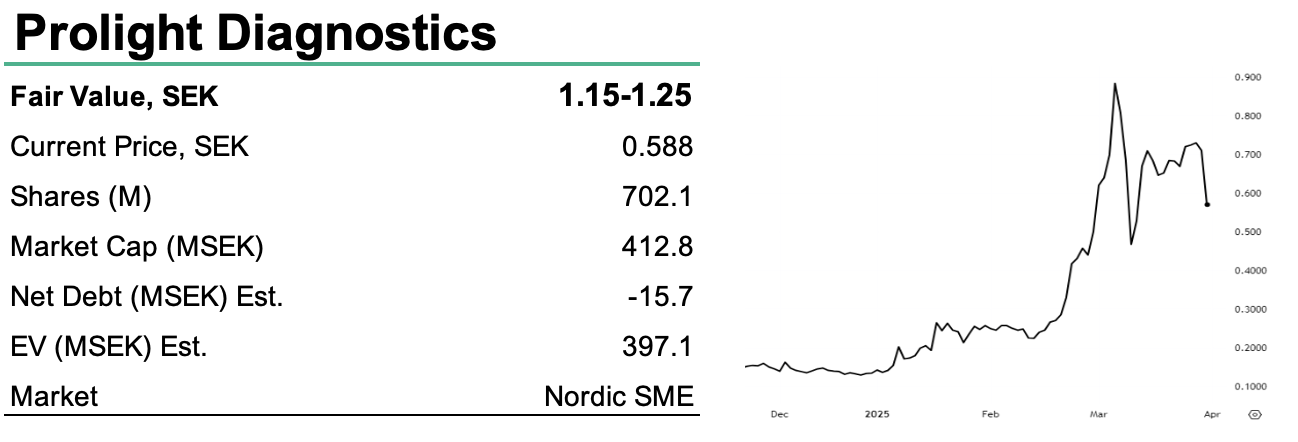

At the end of Q4’24 Prolight held SEK 15.7 million in cash. In addition the company will continue to receive additonal money from the Product Development Award (PDA) received in May 2024 of SEK 17m. In addition the company will, as last year, receive R&D tax credit in the UK, which in 2023 amounted to approximately 7,6 MSEK. Given the annual OPEX run rate of SEK >60 million, financing will become an issue, as current funds are insufficient to support operations through the multicentre clinical performance trial. Ideally, the positive pre-clinical study results could serve as a pivotal stepping stone towards securing an industrial partnership, potentially tied to milestone-based funding. Otherwise, we expect an equity raise—particularly considering the share price has surged some +300% year-to-date, making it an opportune moment to raise capital. With the potential expansion into BNP and D-Dimer POC tests, our rNPV model, rolled over into 2025, stands at SEK 915m. Factoring in an estimated equity raise of SEK 90m, this supports a fair value of SEK 1.15-1.25 (0.9–1.0) per share.

EUR 138m for SpinChip in pre-clinical evaluation

In January, one global in-vitro diagnostics leader bioMérieux announced the acquisition of SpinChip, a Norwegian POC diagnostics benchtop platform for rapid in-vitro testing, for a total enterprise value of EUR 138 million (approx. SEK 1.6bn). The acquisition took place while Spinchip was in pre-clinical evaluation. This and other recent transactions highlight the strong industrial interest in POC systems. Applying a similar takeover scenario to our valuation model—where the business is not weighed down by royalty or milestone obligations but assumes a higher risk for the acquiring entity—supports a valuation of USD 160 million (SEK 1.6 billion), translating to SEK 2.3 per share.