Johan Widmark | 2025-02-14 08:00

Small signs pointing towards a system-wide deal in India

At the presentation of the Q4’24 report, Crunchfish reports of ongoing dialogues in India regarding the RBI’s Digital Rupee, as well as with commercial banks—most notably IDFC First Bank—where the imminent shift from digital copies of banknotes to value-based tokens represents an alignment of the digital payments framework with Crunchfish’s approach. Crunchfish is also pursuing a deal with the National Payments Corporation of India (NPCI, an umbrella organization for retail payment and settlement systems in India), where Crunchfish Digital Cash complements NPCI’s existing offline payment solution, UPI Lite X, with a secure and device-agnostic solution. Interestingly, a new tender—excluding V-Key, which provides the bank-grade security infrastructure in Crunchfish’s existing Digital Cash solution—allows NPCI to implement a proprietary security shell, potentially signaling a path forward toward a system-wide deal in India.

Cash burn at SEK 35m in 2024

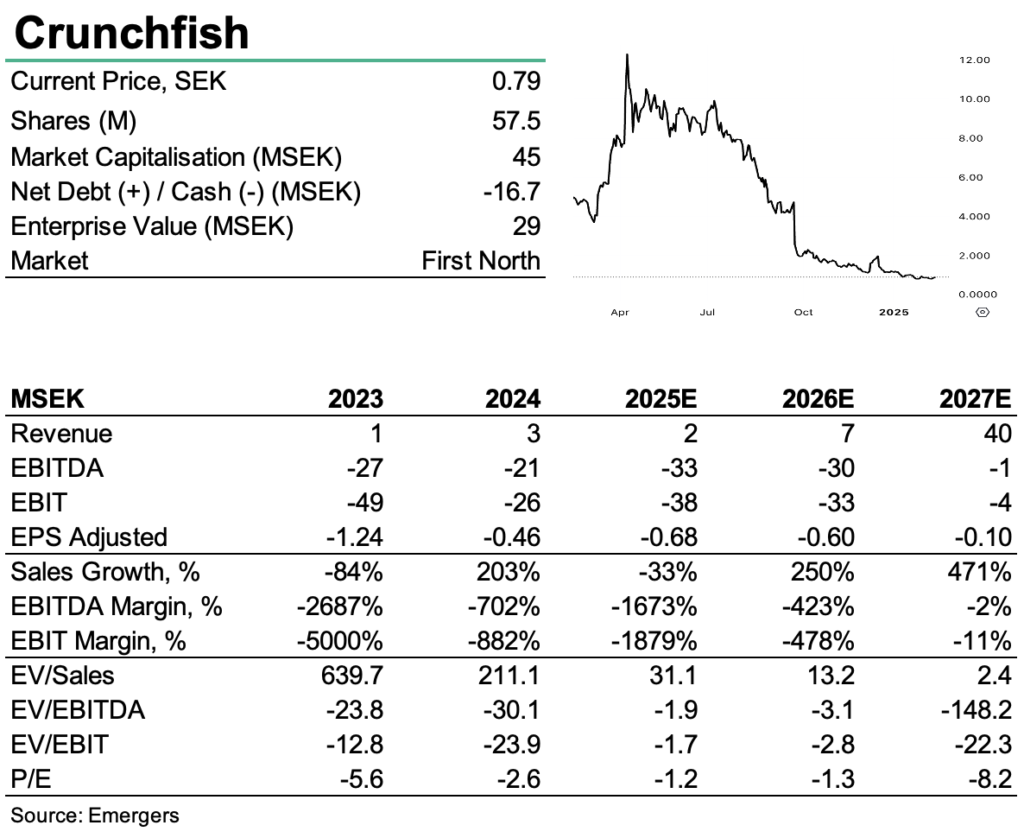

Following the rights issue in November last year, year-end cash amounted to SEK 17m. This is below the annual cash burn rate (FCF) of SEK -35m in 2024, although TO10 could provide an additional SEK 5m (with TO11 expected to be in a similar range) during H1’25. Absent a commercial deal with a significant upfront payment during the course of 2025, we anticipate that additional funding will be needed toward year-end before the long-term potential has a chance to materialize in the P&L.

Characteristics of an OTM option

So, is it possible to assess a fair value for Crunchfish’s share? Any assumptions about future deals, revenues and timeline are highly speculative and uncertain, and there are many possible scenarios. However, some rough assumptions can give an idea of what one of these scenarios could look like. If we model a value capture corresponding to an average revenue of SEK 2 per user, 250 million users by the end of 2030e, a 20% discount rate, a 5% terminal growth rate beyond 2030, a 25% overall likelihood of success, SEK 60m in additional equity capital to fund operations in late 2025/26, and the full exercise of warrants (8.9m new shares for TO10 and TO11, respectively), this would translate to a risk-adjusted Net Present Value (rNPV) of SEK 1.7 per share. Assuming a higher value capture of SEK 3 per user at full roll-out would raise rNPV to SEK 3.4 per share. But this is just one scenario, and there are many other ways this could play out. All in all, we find that the case is now starting to take on the characteristics of an out-of-the-money option, while commercial discussions show some slight indications of potentially moving in Crunchfish’s favor.

Read Crunchfish’s report for Q4’24 here

Watch the full year report webinar here

DISCLAIMER